USD: The Truths Hurt

In this note, I’ll discuss:

The USD bounce - which I see as a lull that led to a position unwind.

Sabotaging the USD revisited - I review the bear case for the USD.

Tariffs and Immigration policy - I view these as brand damage and a productivity hit.

EMFX - dangerously low risk premium, but frequent TACO opportunities.

The Eye of the Storm

After a month or more of marinating in benign US data and falling tariff uncertainty, markets were given a dose of reality at the beginning of this month, first from record payroll revisions, then from the firing of the head of the Bureau of Labor Statistics. The resilience in hiring was revised away, and that inconvenient truth was too much for the President, who prefers his truths with more CAPS.

In July, we saw speculative short USD positions liquidated, and a US equity market, led by tech, rising to new highs. As damaging tariff uncertainty appeared to be sliding towards resolution, the prevailing USD bearish narrative was fraying. For some, the pre-inauguration views were being dusted off. The core of that was higher for longer US rates, with tariffs seen as a US consumption tax hike plus a global growth hit delivered asymmetrically towards the rest of the world. US fiscal stimulus (via the post-inauguration tax bill) would support US growth expectations, and the Fed would keep the USD as a mid-high yielder among DMs.

In a sense, the BLS episode encapsulates the era we're navigating. Beneath each brief period of calm lies another potential shock: political, economic or institutional. Tariffs will never be truly settled, and the underlying economic reality will remain chaotic. Risk assets, meanwhile, have rallied behind a speculative veil, buoyed by the narrative that AI-driven equity gains signify imminent productivity miracles. Yet, bond markets remain sceptical, with elevated term premia casting doubt on the extent to which the real economy will feel the benefit.

So-called "victories" in recent trade negotiations mask underlying structural erosion: tariffs are imposing regressive taxes on US consumers, exacerbating inequality, and therefore undermining the long-term stability of the nation. The White House is chipping away at US soft power and at the institutions that help give the US its exceptional economic standing.

Right now, we’re in the eye of the storm, the post Liberation Day volatility has ceased, the USD has recovered some losses and investors are pausing for breath, and some are bracing for what comes next. This note explores precisely this disconnect as speculative and political veils distort market signals, suppress volatility, and misprice fragility. EM FX investors may wonder why an emerging markets strategy note continues to devote so much time to the United States. The reality is that, for now, there is an orange orb around which EM FX orbits. The instability Trump creates is defining the global opportunity set, and even at a country level, he has the capacity to move the price. I will discuss specific EM opportunities, but with the first principal component dominating, those views are several sections on.

Sabotaging the USD Revisited

When I wrote "Sabotaging the USD” early this year, I argued the Trump administration was intentionally or otherwise undermining the fundamental pillars that supported the dollar's long-term appreciation. As the USD sell-off pauses, it’s worth revisiting the core arguments and marking them to market.

I’ll pick what now seem to be three core areas: US asset positioning overweights, erosion of US soft power and institutional credibility, and shifting relative cyclical dynamics.

Asset Positioning: The global US overweight

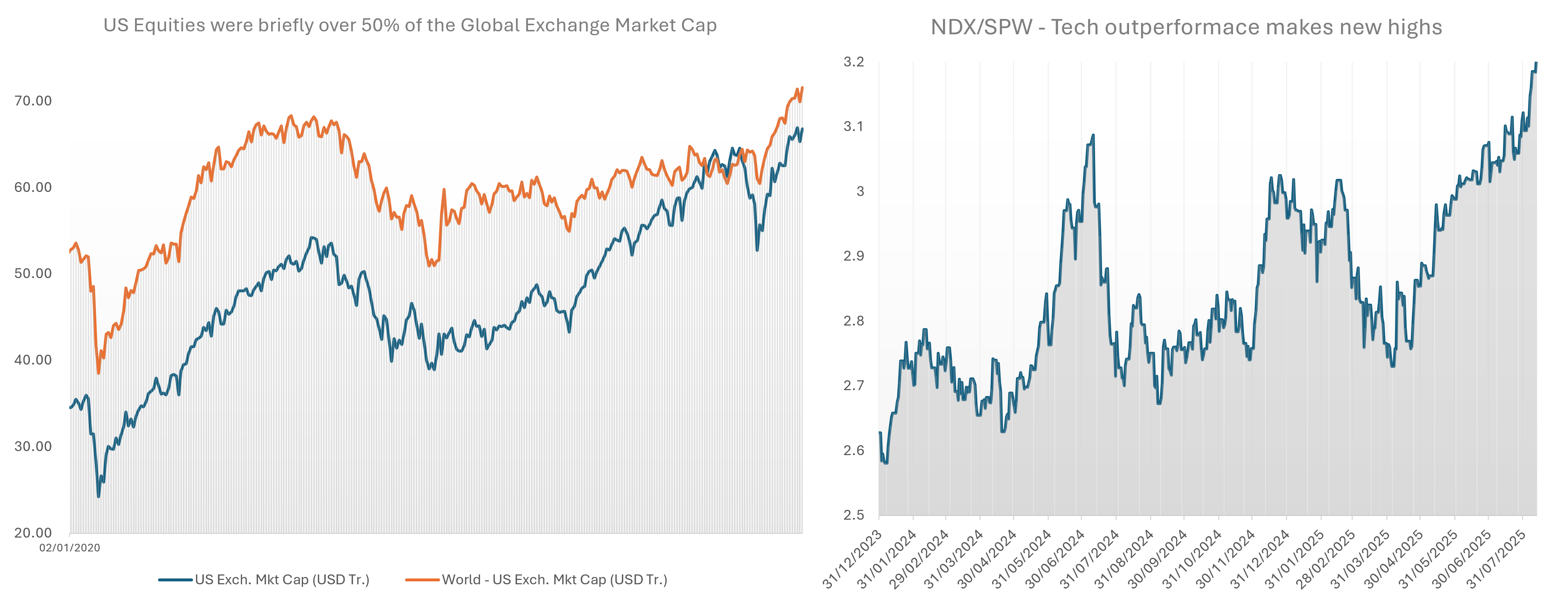

US equity performance and inflows post-pandemic took the US share of global equity market cap above 50%. Large passive investors have allowed themselves to be overweight the US, and Liberation Day was a moment for reassessment. At the same time, the yield differential over most Asian currencies meant that USD holdings represented an attractive carry trade.

During April and May, US overweights were frantically hedged. Taiwan was the poster child of this flow. The failure of the USD smile to materialise during a crisis that was made in America eroded another pillar. The recent USD stability gives pause, but a full rebuild of that USD exposure seems unlikely, I would expect further trimming. US equities have staged a recovery, but it’s increasingly narrow. The only exceptionalism doing the lifting is tech. Anyone wanting AI exposure will likely buy US-listed names and this will keep a structural bid under USD assets for as long as the trend continues, or the bubble inflates depending on your viewpoint. This is one of the main tensions in the USD outlook.

Institutional and Soft Power Erosion: Waves of damage

Trump 2.0 opened with a volley of self-inflicted blows to US soft power. Early trade and security jabs at allies will leave a mark. Temporary calm from tariffs and NATO deals won’t last. There is no post-victory calm for Trump; he needs to keep the headlines rolling. Domestically, the attacks on institutions continue, with the Fed under pressure, and the BLS chief fired for delivering data that clashed with the preferred narrative.

Relative Cyclical Dynamics: The tough call

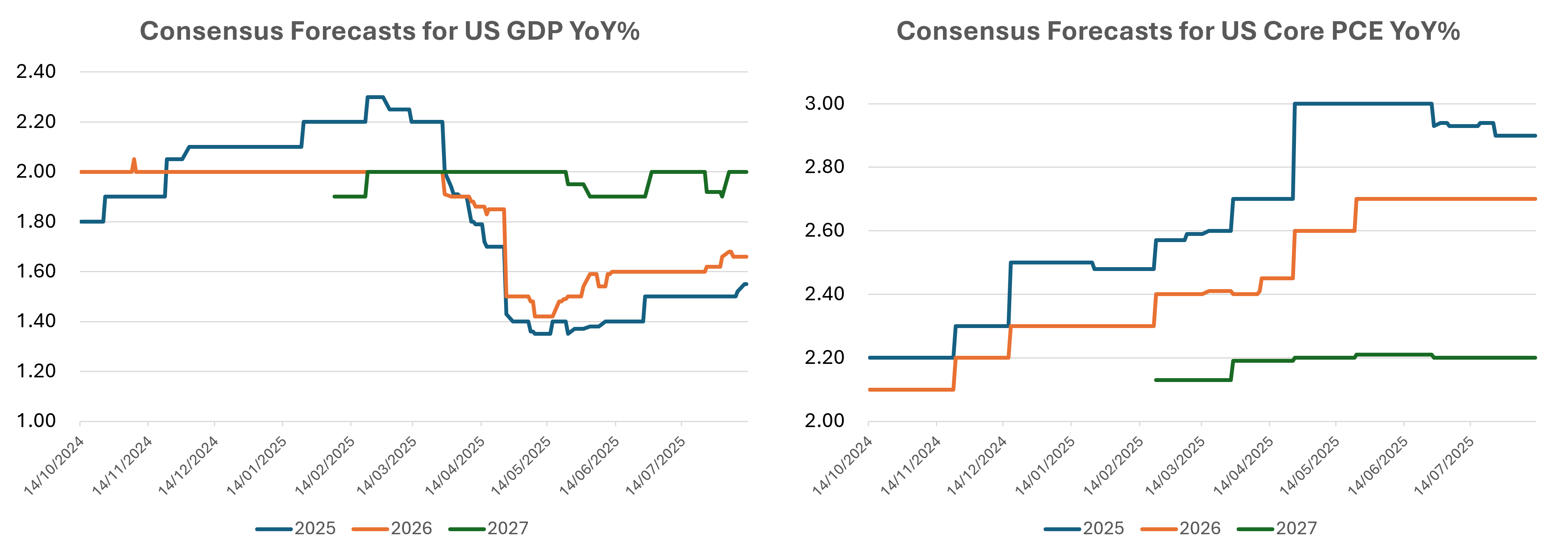

The macro read is still murky. Equity-driven easing in financial-conditions measures can make nowcasts and survey composites look better than the real economy, so the headline signal is flattered. Labour market weakness could be a short-lived tariff shock or the start of something deeper. Hiring has slowed, but layoffs haven’t accelerated. Consumption is soft, yet real wages and employment levels remain intact. Economists have eased back some of their growth downgrades, betting the shock will be spread over time. The latest payroll data tilts the risk back toward renewed USD weakness, but this is the hardest variable to price: the cycle could just as easily stabilise as roll over. What does seem clear is the asymmetry expected is not there: the hit to US growth expectations has been harder than we’ve seen in the EU or China, with the latter looking firmer than pre-Inauguration.

Trump’s Tariff Playbook and the Myth of Strategic Victory

Any USD strength on the notion that trade agreements represent a strategic victory is off base. I don’t think this can be called out strongly enough. These tariffs are politically expedient populism, not strategy, and they cause structural harm. Trump sells them as tools for reindustrialisation and a manufacturing renaissance. In reality there’s no coherent industrial policy. They aren’t foreign-funded either. The bill lands on US consumers and SMEs, with near-total pass-through to prices. Lower-income households carry more of the burden, small businesses lose competitiveness, cut investment, and the inequality gap yawns wider. That kind of regressive tax weakens the structural soundness of the US rather than strengthening it.

What hurts the USD is the chipping away at the trust and cooperation that underpinned US soft power. Allies now see the US as unreliable, and will hedge with new trade and security arrangements that will, over time, dilute American influence. The starkest own goal was the foreign-aid rug pull. Funding was yanked, pipelines broke, vaccines expired, and food programmes evaporated. Gratuitous harm for domestic theatre, and abroad, it looked like abandonment. That is how you squander decades of goodwill in a month.

What Real Strategy Would Look Like

A credible China-containment and re-industrialisation agenda would rest on three pillars:

Human capital - sustained funding for technical colleges, apprenticeships, and mid-career re-skilling aimed at fabs, advanced packaging, grid engineering, and precision machining.

Capital formation - multi-year tax credits and direct grants that de-risk private investment in semiconductor plants, battery supply chains, and transmission infrastructure; incentives sized to match the cap-ex curve, not the news cycle.

Allied alignment - tariff and export-control policy set in concert with Europe, Japan, and Korea, minimising retaliation risk and maximising collective leverage over China.

Get those three right and the US has a strategic industrial policy rather than a sequence of ad-hoc measures. Biden’s IRA and CHIPS Acts point in the right direction, but the Autopen needed to be on a bolder setting. Trump could, in theory, have used his political capital to amplify this framework; instead, the emphasis shifted back to headline tariffs and bilateral theatre. Strategy gave way to optics.

Immigration: the silent partner of US exceptionalism

In recent years the US has benefited from a common EM phenomenon. In China, three decades of rural-to-urban migration kept unit labour costs contained while factories scaled. The hukou system slowed wage catch-up in the cities. Cheap, elastic labour was the shock absorber that allowed capex to boom without immediate inflation. Mexico’s post-NAFTA manufacturing corridor used northbound migration and internal mobility to hold down wages relative to productivity.

Many EMs operate with thinner safety nets. The US achieved a similar effect by virtue of the status of much of its immigrant workforce. A deep labour pool let firms hire fast in upswings and release in slow patches without shifting the cost to the state. That kept services inflation lower than otherwise and helped the post-pandemic recovery run hotter with fewer people stuck on the sidelines. Set that beside Europe, where labour markets are tighter and the state absorbs more volatility, and the US enjoyed a cleaner growth-inflation trade-off.

The new administration is taking that buffer away, sharply. Hiring slows and gets pricier unless growth rolls over. Wage pressure shows up in construction, food, care, hospitality and logistics. Productivity still arrives, but diffusion slows: labour frictions and higher unit costs sit in the very services that dominate modern GDP.

Part of the dollar’s appeal is a flexibility premium: an economy that can move people quickly and absorb shocks with less fiscal strain. Undermine that and the US starts to look more like its peers; the growth and inflation edge over Europe erodes.

It’s Raining EM TACOs

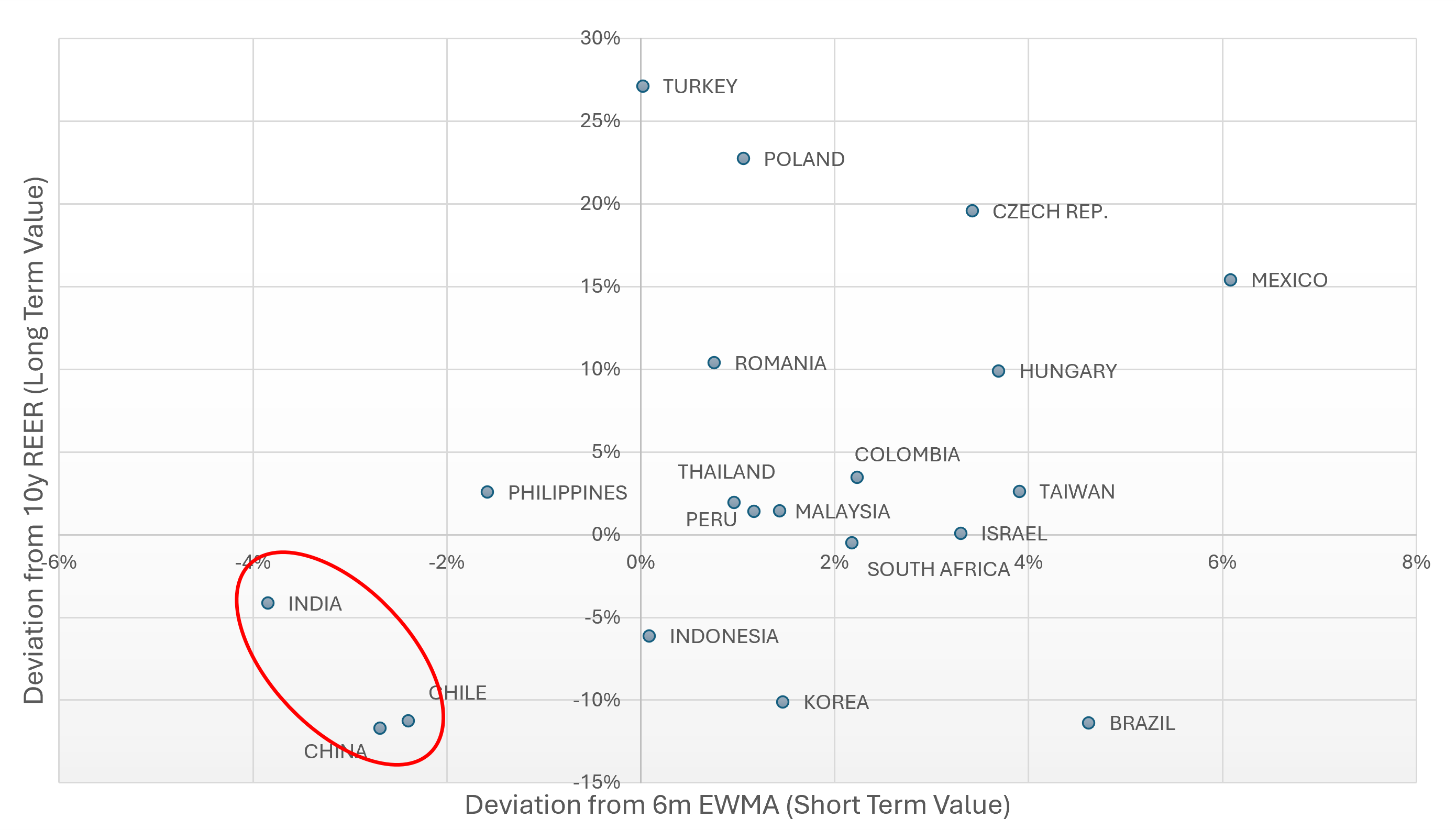

My base case is for another leg of USD weakness. The main risks are the US cycle and AI-driven US Tech investment flows. Broadly, EM FX is helped by gradual USD weakening in the absence of volatility spikes. Given the current elevated equity valuations and tight credit spreads, risk premia are thin. With that in mind a safer way to express a USD short would be via currencies that are clearly structurally undervalued.

There is real value in parts of EM. China, Brazil, Chile and Korea screen as cheap on longer windows. India and the Philippines lean cheap on shorter windows. CEE and Mexico screen rich on both axes. The currencies that have lagged recently and remain structurally cheap are INR, CLP and CNY. The last of those is at the whim of official policy, and I expect the Chinese to continue to guard their competitiveness in the face of deflationary forces. Chile has taken the unusual step to rebuild reserves at a time of low valuation. For me, this means that the opportunity is more limited, and possibly one for a ratio option structure, playing for partial normalisation. India is most interesting and plays into the TACO theme.

TACOs in EM

The pattern is familiar now: headline shock, politicians posture, costs hit, carve-outs and delays follow, FX mean-reverts.

We saw this play out with China. The domestic economic cost was too high, which led to pauses, phased roll-ins, and a scaling back of the policy.

In Brazil, we have a good blueprint. The headline tariff shock pushed BRL weaker. Lula stood up to the bully, then Washington watered down lines that mattered for Brazil. The currency retraced.

India is the current candidate. We have already seen chatter of US product boycotts. The cost of broad US tariffs would hurt both sides. I would suggest that once more, exemptions, phasing and a backtracking are on the menu. India’s macro outlook is solid, with the current account deficit below 1%, which is small relative to its history. Growth expectations have stabilised after last year’s wobble. Reserves are ample.

The point is simple. In a world where tariffs are theatre, TACOs become a feature of trading EM FX. Wait for the sell-off, position for the climbdown.

Closing Thought: The Truths Hurt

Few positioned for the Q2 USD sell-off, yet many were caught short in the recent consolidation, FX is tough. We have discussed the key cross-currents: a murky US cycle and AI-led US equity inflows. What seems the more structural medium-term reality, though, is the persistent sabotage from the White House.

The hard truth is that tariffs are a tax on your consumers, not a strategic victory. Allies are being needled, not aligned. Institutions are being leaned on, not strengthened. The immigration buffer that kept services inflation tame is being stripped out. Each of these chips away at the growth and credibility premia that have underpinned the dollar.

The United States is being led by a keyboard warrior. When it comes to the dollar, the truths hurt.

Signing off

Thank you for your time and attention. Please feel free to reach out with any feedback.

I continue these ad hoc notes to help organise thoughts, keep in touch with a wider community of like-minded investors. And for the sheer pleasure of writing.

As always, if you’re trading, be disciplined and be lucky.

Stephen

Disclaimer

The contents of this note, including any analysis, opinions, and commentary, are purely for informational purposes and reflect solely the personal views of the author, Stephen Elgie, at the time of writing. They should not be construed as investment advice nor as an inducement, recommendation or solicitation to engage in any form of currency trading or other investment activities.

All information, data, and material presented in this note are believed to be accurate and reliable, yet they are not to be taken as a guarantee of future performance. The views expressed herein are subject to change without notice.

Readers are urged to exercise their own judgment and due diligence before making any investment decisions. The author and his employer, Argo Capital Management Limited accept no liability whatsoever for any loss or damage of any kind arising out of the use of all or any part of this material.

This note is not intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation.

Thanks Stephen