The China Manufacturing Gravity Well

Prospects for Emerging Markets under a new China regime

The ageing reflex

China’s manufacturing success is creating gravitational forces that are reshaping the development paths available to EM economies. In this note, I’ll unpack what that means.

Earlier in my career, there was a safe reflex toward China. Watch lending data, keep an ear to the ground on policy, and on any sign of an acceleration in China, buy EM assets. We all understood the transmission mechanism well. Chinese growth upswings were driven by property and infrastructure booms, which pulled in commodities, machinery and other capital goods. As a result, much of the emerging world experienced a boost to demand. Time it right, and you had a career.

Some years ago, that relationship weakened. After the property downturn, the way that growth connects to the rest of EM has changed. The new pattern is less supportive, with China sustaining activity more through manufacturing scale, and the adjustment being pushed outward through surplus supply and tougher competition in tradable goods.

This is well reported, but mostly as a developed-market problem. We’re familiar with the arguments about tariffs, ultra-competitive electric vehicles and solar, and how they shape industrial policy in Europe and the United States. As an EM investor I want to discuss what it means for the countries in the middle. Many EM economies do not have the market size, fiscal capacity or policy room to respond effectively.

The harsh truth is that China’s success has changed the opportunity set for others. Manufacturing was the most common route through which earlier Asian economies escaped the middle-income trap. For much of EM, that route now looks increasingly narrow. China’s scale, pricing pressure and supply-chain depth are compressing the space available to EMs that wish to follow that path. The consequences are significant for medium-term growth quality, current account durability, and the country-level dispersion that increasingly drives differentiation in EM local assets and FX.

The old playbook has died. The replacement needs a better mental model.

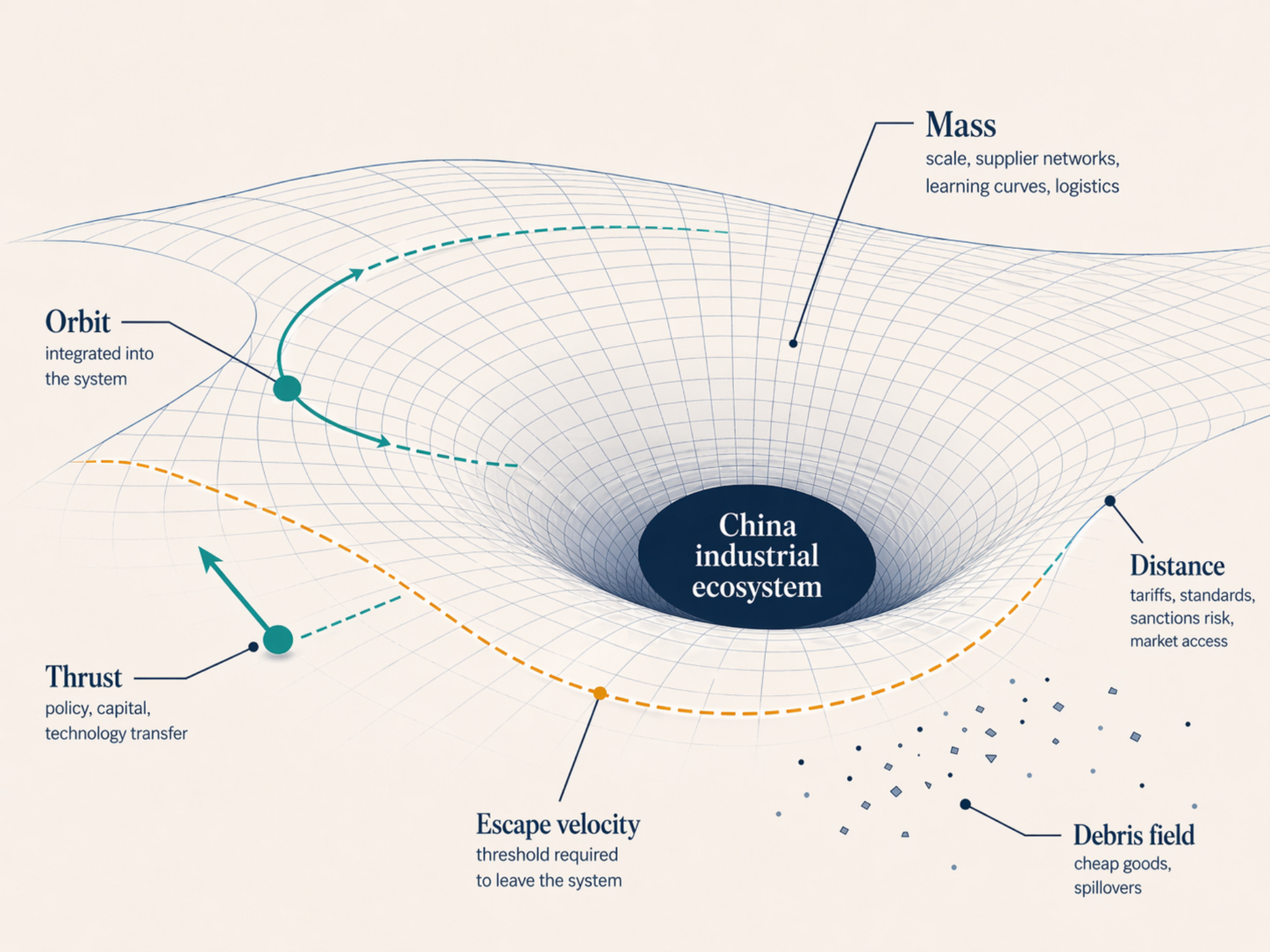

The gravity well

As a former physicist, the metaphor I’m drawn towards for the new China-EM transmission is a gravity well. In physics, a gravity well is a way of visualising gravitational potential. A sufficiently large mass creates a dip in the field. Where in the past we thought of objects as being “pulled in” by some special force, thanks to Einstein, we now think of them as following the shape of the field. If they do not have enough energy to escape, they remain bound to it, often in orbit. For the metaphor to earn its keep, the terms need to be precise: mass, distance, thrust and escape.

In this context, the mass is China’s industrial ecosystem. The point goes well beyond low wages or marginally cheaper production. The learning curves were climbed years ago, the supplier networks are dense, and the state can keep capacity alive through periods of weak profitability that would shutter plants elsewhere. Any country trying to compete in that environment is up against a whole industrial system. Distance is not mainly geography. It is economic distance. Tariffs create distance. Standards create distance. Rules of origin create distance. Sanctions risk creates distance. Market access creates distance. EU membership is a form of reduced distance to one industrial bloc and increased distance from another. USMCA does something similar.

Thrust is the set of forces a country can apply to change its trajectory. Policy continuity matters. Capital deepening matters. Technology transfer matters. Security cover matters. Most of all, access to a large final-demand market that is not China matters. Without some combination of those, countries can integrate into the system but struggle to alter the terms of that integration. Thrust, in short, is what most EM countries have just enough of to stay in orbit, and not quite enough of to leave it.

A gravity well is not a black hole. I don’t want to provoke the image of countries crossing an event horizon and journeying to economic oblivion. Orbit can work. That is part of the trap. Countries in orbit can still grow, export, industrialise at the margin and at times perform well. However, the danger is shrinking autonomy and capability over time.

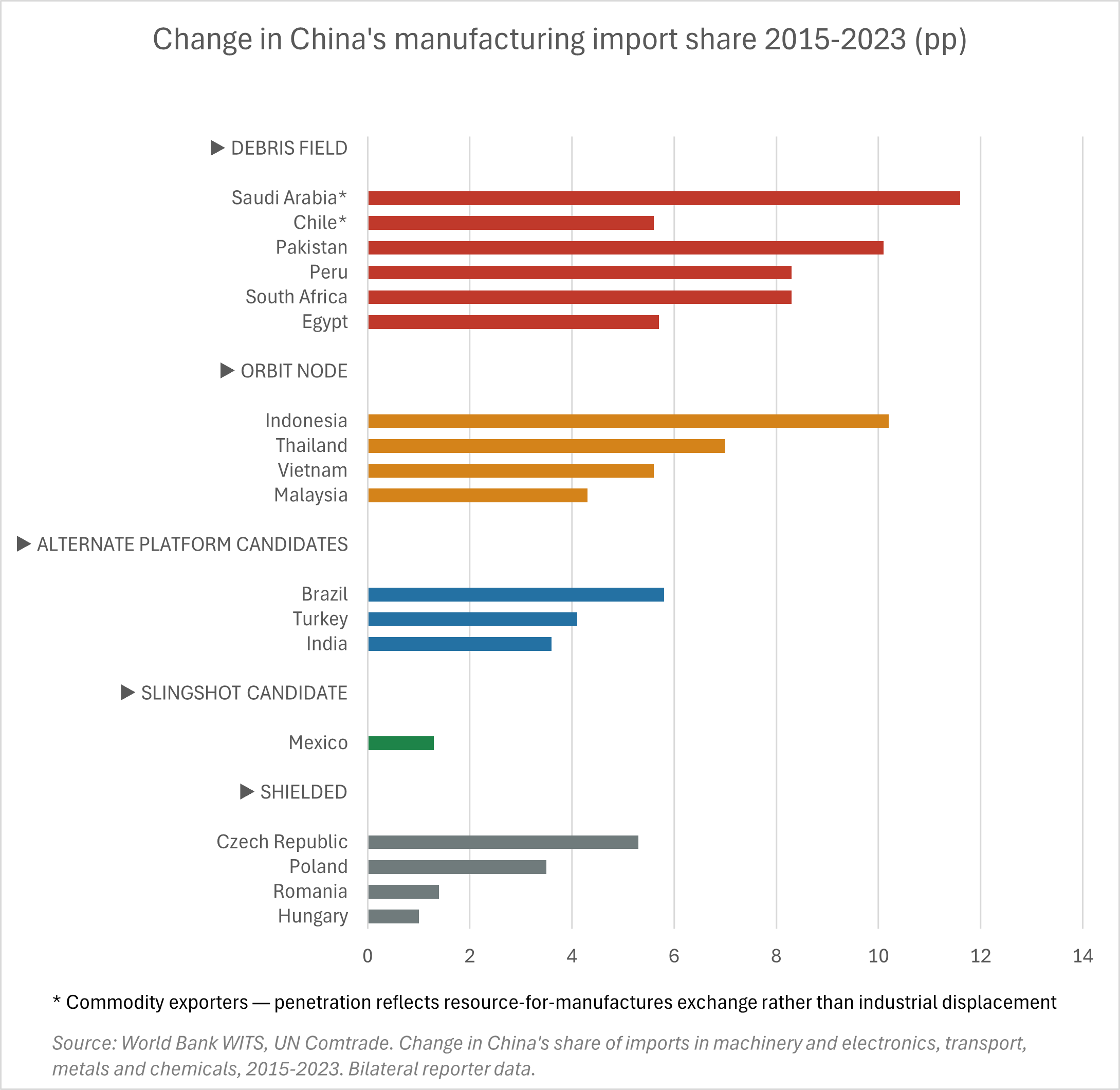

A slingshot candidate is a country with privileged access to a large non-Chinese market and enough thrust to move beyond node status. A shielded economy is protected by deep institutional integration into an alternative industrial ecosystem, effectively operating inside a different well. An orbit node is a country that operates inside China-centred supply chains but struggles to ascend the value chain. A debris field country is one showered with cheap goods but whose own industrial ladder never properly catches light.

China is not the only gravitational mass in the system, but it is the fastest growing and the newest force. The US and the EU create their own wells, with their own barriers and internal protections. But any barriers they erect merely redirect the impact of China’s industrial force. Output that is prevented from entering developed markets is pushed elsewhere. This is particularly toxic, as it accentuates the debris-field problem at the EM periphery.

The engine change

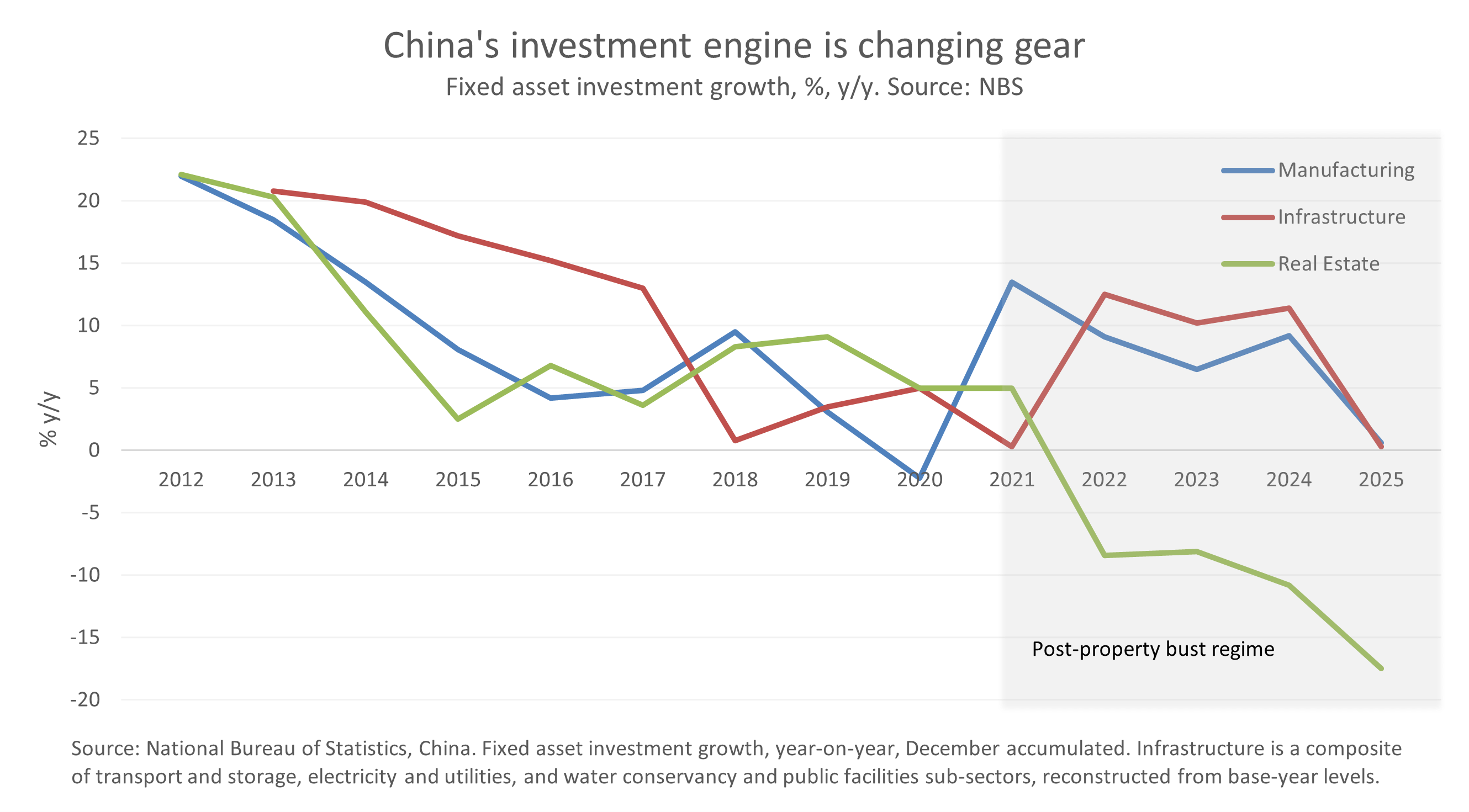

The old Chinese growth model used debt expansion to keep domestic activity high, whilst pulling in demand from the rest of the world. This delivered impressive GDP figures but also a level of development sufficient for the social contract. The country was upgraded around its citizens, as they enthusiastically ploughed savings into an appreciating property market. Wealth effects and rising living standards compensated for visible constraints on personal and political freedoms. Property, a cornerstone of the model, broke decisively in 2021, marked by the Evergrande collapse. Nearly five years on it shows only tepid signs of recovery.

Decades of investment have seen China’s transport and energy infrastructure in its major industrial corridors become world class, leaving limited room for incremental productive investment. On the initial lurch lower in real estate, infrastructure investment was well calibrated to provide a temporary bridge, with manufacturing investment also providing support. The striking feature in the latest data is that all three major investment channels are sagging at the same time. GDP has held up in the aggregate, with past investment having built the capacity to deliver on growth targets with net exports picking up the slack. The balance is fragile. As domestic investment loses force, the pressure shifts further towards utilisation and output.

Manufacturing is the engine that’s still firing, and has played a key role in powering China through the property collapse. The issue for the rest of the world is what a powerful industrial system does when domestic demand is too weak to absorb what it can produce. China does not need to keep building the well deeper. The mass is already there. The question is what that capacity is producing, and where it is going.

The mass accumulates

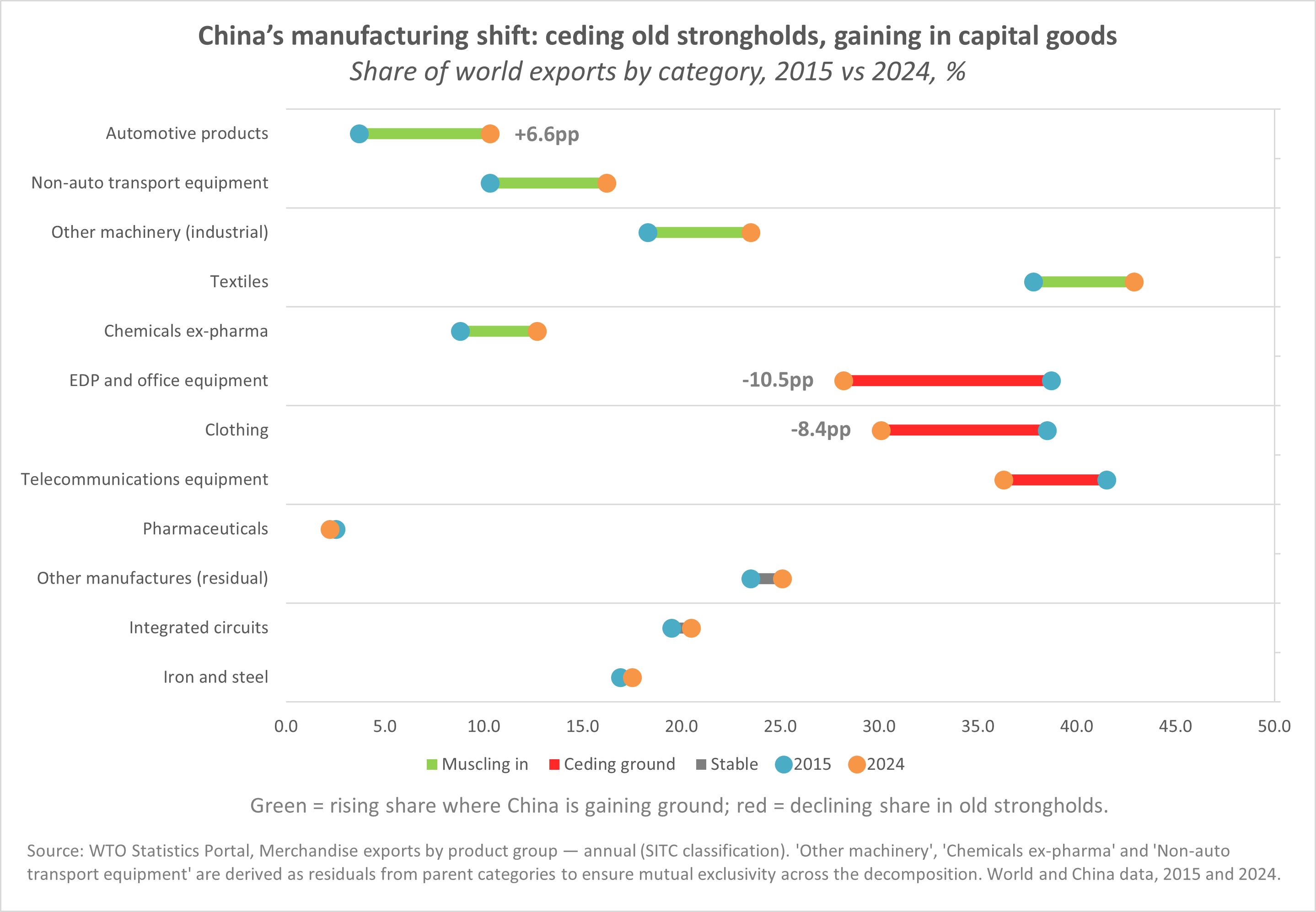

China’s share of world manufactures exports has moved in a fairly narrow range over the past decade. However, since Covid, China’s export machine has looked much more forceful: volumes are up, the manufactured goods surplus is much larger, and imports have been much less impressive. China is pushing harder, and the push is moving into sectors that matter more for EM industrialisation.

Automotive products are the standout case. China’s share of world automotive exports rose from 3.7 per cent in 2015 to 10.3 per cent in 2024, catapulting it into the trophy sector of global manufacturing. Non-auto transport equipment and industrial machinery tell a similar story, with world export share rising from 10.3 to 16.2 per cent and 18.3 to 23.5 per cent respectively. By contrast, sectors where China is already well entrenched have seen share drop off sharply. Most notably electronic data processing, telecommunications equipment and clothing.

The relevant point for EM is compositional. The pressure is strongest in areas that matter more for the next stage of industrial upgrading. In Chinese discussion this dynamic is often described as neijuan, or involution: competition so intense that firms keep cutting costs and running harder even as margins compress. This is why Chinese export pressure now lands in the sectors many EMs hoped to enter.

Exporting the adjustment

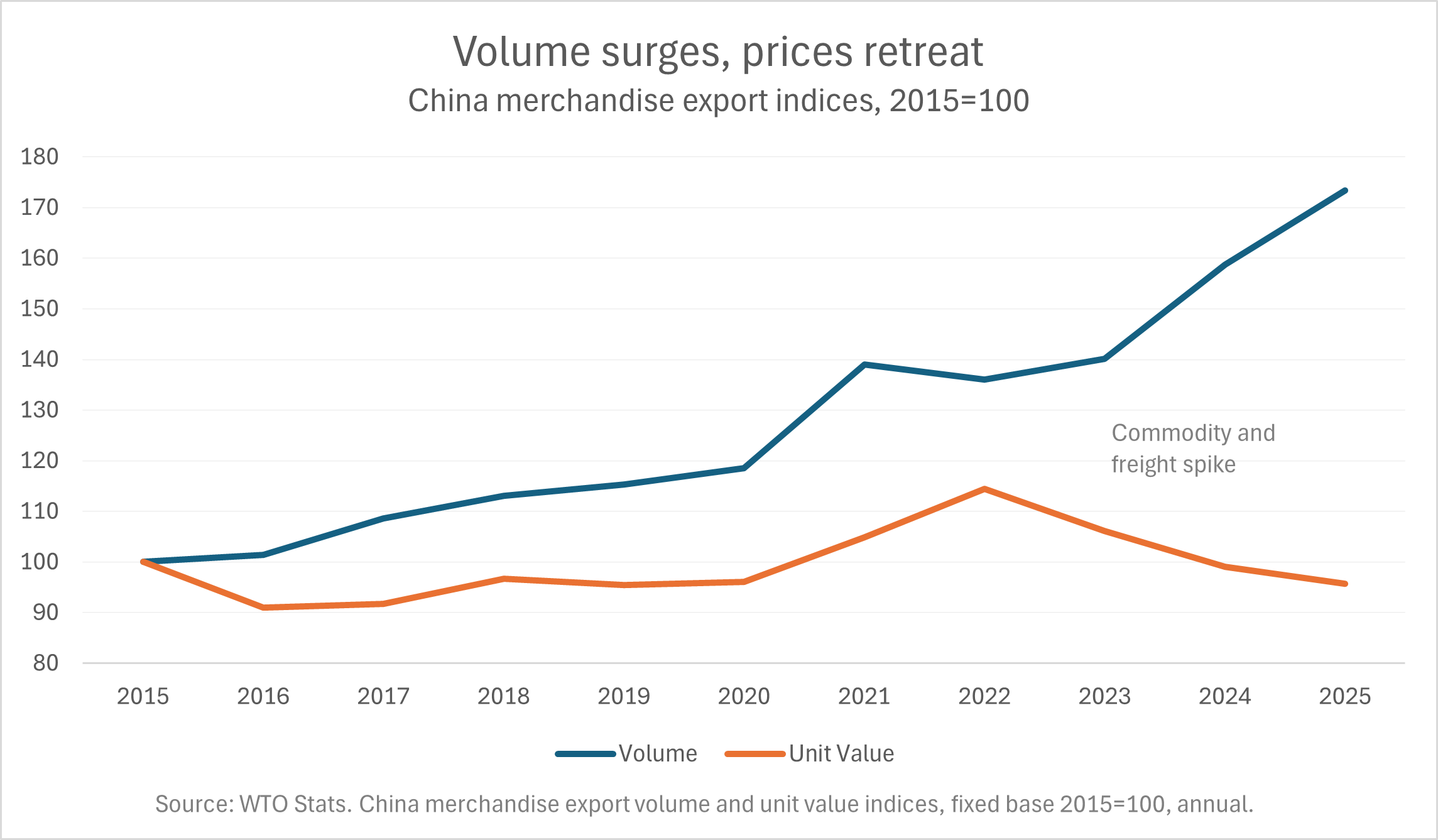

China’s merchandise export volumes rose 73% between 2015 and 2025, while export unit values fell 4% over the same period. More quantity is leaving the system, at lower prices than a decade earlier. The 2022 spike in unit values was commodity and freight. Once that faded, the structural signal reasserted itself.

Local governments, in addition to having output targets, collect VAT at the point of production. This means they are given powerful incentives to keep factories operating. Capacity that would shrink more quickly in a normal market setting can remain in operation for longer. Cheap financing and that “famously competitive” exchange rate reinforce the same outcome. The result is a system in which weak domestic demand does not lead cleanly to lower output. It leads more often to output being pushed outward.

It’s worth going deeper into the potency of neijuan, or involution here. China has produced a system where competition is so intense that firms are forced into a near-continuous cycle of cost cutting, process improvement, automation and product iteration. Firms that survive inside that system emerge faster, leaner and more adaptive than rivals operating in calmer markets. They learn to redesign quickly, source more efficiently, compress lead times and strip cost out of production with unusual speed. The result is an industrial base with a kind of brutal potency: a domestic arena so competitive that surviving it becomes, in effect, a training ground for global dominance.

The state has initiated the process and fuelled it with subsidies. In a normal market, competition this brutal would eventually clear the weaker players and allow margins to recover. China’s system and its incentives make this cleansing difficult and slow. As a result, excess capacity stays, and the pressure has nowhere to go but out.

One Chinese sensor manufacturer saw its unit price fall from around $30 to under $2 in five years. The rate at which its competitors improved must have left the owners’ heads spinning.

The micro version of the chart plays out among Chinese producers in sectors tied to the EV supply chain who have seen selling prices collapse over a few years, as competitive conditions left them little choice. Quantities keep rising. Margins get squeezed.

For EMs, competing on cost alone is an empty pursuit, with the cost floor moving down. The same process has produced some real gains for some trading partners. Cheaper solar and battery technology benefits energy importers and electrification programmes. The distribution matters. Some countries get cheaper inputs. Others get their industrial margins crushed.

My overriding message is that the sectors under the greatest pressure are the very sectors middle-income economies would normally target in order to become richer. Autos, machinery, batteries, electrical equipment and the broader tradables ecosystem around them are the core route to higher income status. China has successfully industrialised on a scale that will outmuscle most attempts by others to follow suit.

The old China model absorbed external demand and created space around it. The new one sustains output at home and pushes pressure abroad. For countries still hoping to use manufacturing as the main route through the middle-income trap, the reality is beyond disheartening.

Who gets hit

Chinese manufactured goods are not landing evenly across EM. The first thing the data does is sort countries into three broad camps. Some countries are receiving Chinese manufactures as the other side of a commodity trade. Saudi Arabia and Chile sit high on the raw penetration measure, but this is not quite the same as industrial displacement: commodities go out, manufactured goods come back. That still matters for terms of trade, but it is not the same problem as a domestic manufacturing ladder being kicked away.

The more relevant pressure points are the countries where Chinese penetration is rising in sectors where local industrialisation would normally need room to deepen. Pakistan, South Africa, Peru and Egypt sit closer to that debris-field pattern. Consumers quite like cheap goods, as it turns out. The issue is scale and price: whether Chinese supply is arriving at levels that make local alternatives harder to form.

A third group looks different again. Vietnam, Indonesia, Thailand and Malaysia show high or rising Chinese penetration alongside export success. That is the orbit-node problem. Integration into Chinese-centred supply chains can support growth, jobs and exports. It can also deepen upstream dependence. From a distance, both can look like industrial success. The wiring underneath matters.

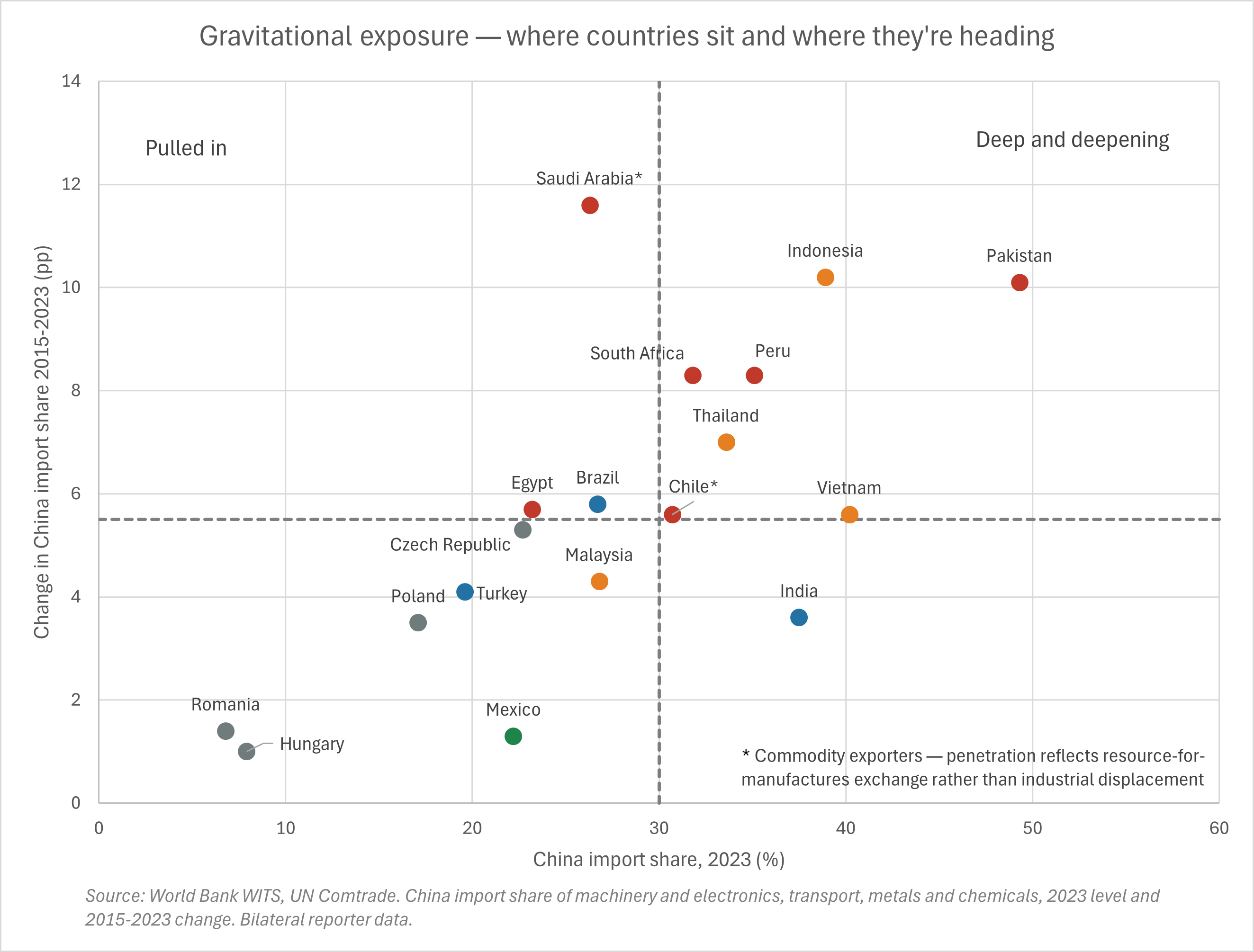

The second view adds the missing dimension: where countries already sit. A modest recent increase can still leave a country deeply embedded, while a large increase from a low base may mean a country is only now being pulled in. On that basis, Pakistan, Vietnam and Indonesia look among the most exposed. Mexico remains unusually insulated. CEE sits lower and flatter than most of the EM universe, with the EU pull visible in the data. India sitting alone tells us a lot. This is the only country large enough to generate enough of its own gravity to stand away from the others.

Rising Chinese penetration can mean cheap finished goods crowding out local production, Chinese intermediate inputs feeding export growth, or commodity exporters recycling their China revenues into imported manufactures. Those are not the same economic story.

What neither chart can tell us on its own is whether rising Chinese penetration is crowding out capability or helping to build it through supply-chain integration. That is the line between orbit and escape.

Orbit or escape

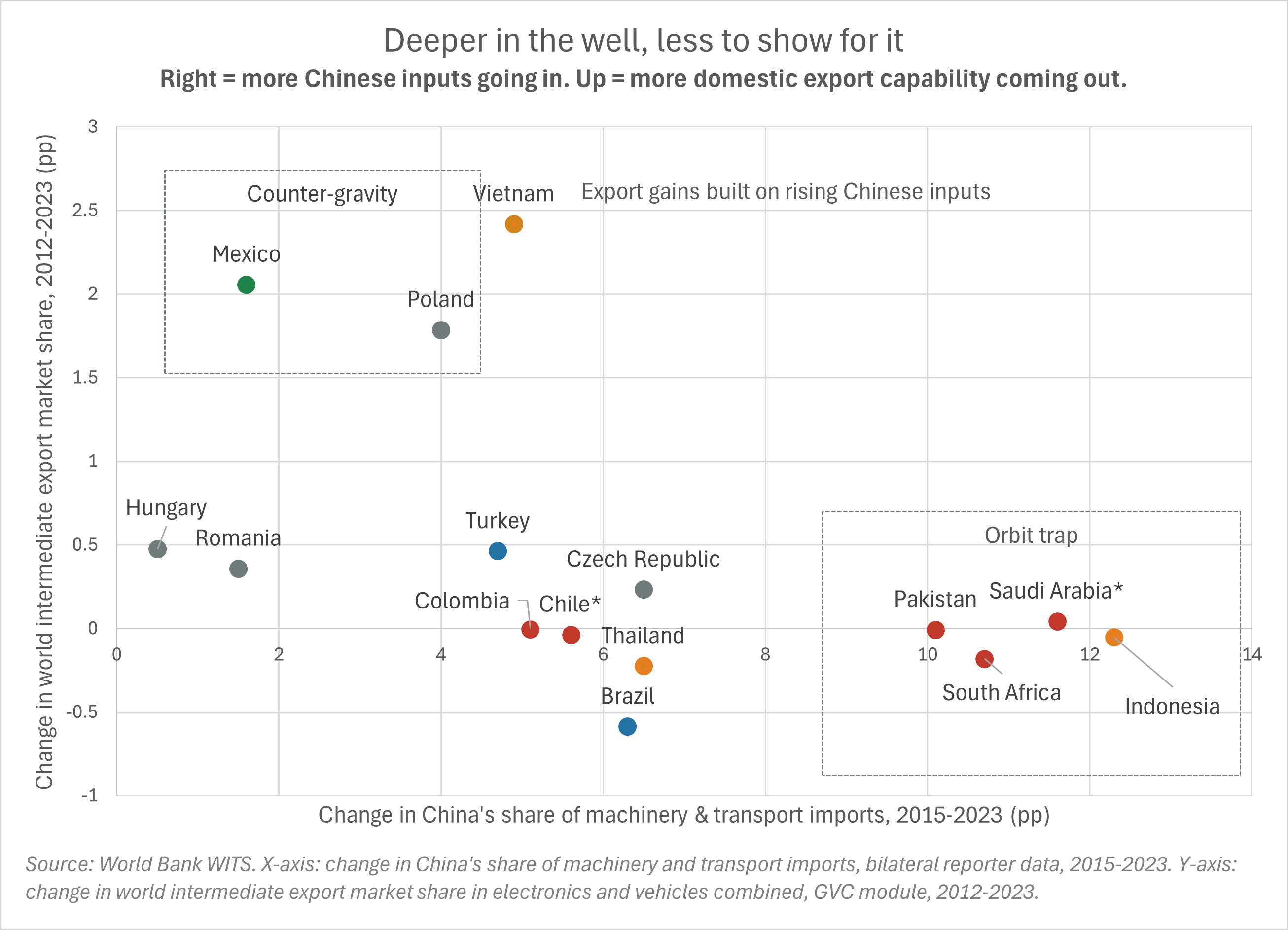

The next test is whether Chinese inputs are helping countries build capability or merely passing through them. Importing from a more advanced industrial base has often been part of the industrialisation process. Countries start by assembling other people’s components, then try to climb into local content, intermediate production, tooling, design and eventually higher-value exports. The question is whether the Chinese supply chain still works that way for latecomers, or whether it now holds many of them closer to the lower rungs.

The chart should be read simply. Moving right means a larger increase in Chinese machinery and transport inputs. Moving up means a larger gain in world intermediate export share in electronics and vehicles. Inputs in, capability out. That is the test.

The pattern is not especially comforting. Indonesia is the cleanest orbit-trap case: more Chinese machinery and transport content coming in, little intermediate export capability coming out. This is different from the debris-field problem, where Chinese goods arrive at scale and crowd out local formation. In the orbit trap, a country is inside the chain but not climbing it.

Vietnam is the awkward case, which makes it the interesting one. Its export gains are real. Some of this may be tariff dodging or transhipment. It would be odd if none of it were. But the gains are not just paper flows. The better question is where the value added sits. Intermediate export share has risen strongly. But those gains have come alongside deeper dependence on Chinese upstream inputs. China’s own move up the ladder creates room for Vietnam to do some of what China used to do. To put it more crudely, how many more rungs can it climb before hitting its head on something hard?

Mexico sits closer to the other end of the field. Chinese input dependence has risen only modestly, while intermediate vehicle export share has increased materially. That looks much more like a slingshot: privileged access to US demand, rules of origin that force local content, and enough industrial base to make the opportunity real. Poland points in a similar direction through European integration rather than USMCA. These cases are rare because the conditions are specific. Access alone is not enough. The system has to force capability to accumulate locally.

Mexico is also a useful warning against getting too excited. Long-time EM investors have seen this film before. Mexico has had a better structural hand than most peers for decades, and yet per-capita income performance has still disappointed. A slingshot position creates the possibility of escape. It does not guarantee that the country uses it well.

Brazil is the warning from the other side. It has scale, a large domestic market and a plausible claim to industrial ambition. Yet in this data it shows higher Chinese input dependence with weak intermediate export performance. Scale helps. It does not create escape velocity by itself. The country of tomorrow can remain the country of tomorrow for a long time; China is not the only reason, but it does not make the climb easier.

The rest of the chart fills in the pattern without needing a country-by-country autopsy. The Czech Republic looks more capable than countries with similar Chinese input penetration, consistent with institutional embedding in European supply chains. Hungary and Romania sit in the more insulated part of the field. One caveat is that gross trade data may flatter the CEE story if more Chinese value added is already sitting inside European supply chains. That is a follow-up rabbit hole, not one to disappear down here. The commodity cases sit near zero on intermediate export gain, which is consistent with the earlier point: this is not their main channel.

Orbit is not a waiting room. It is a business model. Countries and firms adapt around the Chinese ecosystem. They source upstream from China, specialise in assembly or downstream functions, and try to hold margin where they can. That can be rational, profitable and politically attractive for a long time. The question is whether it builds autonomy, or whether it simply teaches the economy to live inside someone else’s supply chain. Politics may not always tolerate this either. In democracies, manufacturing jobs, trade deficits, national champions and foreign ownership can become live issues quickly. Orbit can work as a business model and still become an ugly political story.

India and Malaysia are the two important gaps in the chart. India matters because it is the major large-country attempt at an alternative manufacturing platform. Malaysia matters because it is probably one of the more sophisticated orbit-node cases, with semiconductor strength sitting alongside deep regional input dependence. The data isn’t clean enough to place them with confidence.

This is the distinction the data makes visible. Some countries are taking in more Chinese inputs without building much intermediate capability. Others are using their position to build something more durable. The trajectories are not the same, and the gap between them is likely to widen.

Why escape is hard

The uncomfortable part is that many EM governments understand the risk. They know that deeper reliance on Chinese inputs and capital goods can weaken the long-term industrial ladder. They often deepen that reliance anyway. The reason is not mysterious. Chinese equipment, intermediate goods and financing arrive quickly and cheaply. The alternative requires sustained industrial policy, patient capital, institutional competence and technology access over many years. Most countries do not have a political system capable of seeing through multiple coherent five-year plans.

For a domestic electorate, the near-term gains from integration are visible: lower costs, faster project delivery, export jobs, cheaper infrastructure. The long-term cost is harder to see. A domestic supplier that never forms does not complain. A capability that never accumulates does not show up in the data as a missing factory. The loss is real, but it is politically quiet. By the time a nation is able to look back on disappointing progress the leaders that took the decisions are long gone.

The US is the obvious escape route in theory. It has the market, the technology base, the financial system and the strategic motive to provide counter-gravity at scale. Increasingly the problem is reliability. Tariff policy moves around, allies get treated transactionally, and support for external commitments has become less predictable. That said, the US is not simply unreliable noise. Anti-China policy now runs deeper than Trump. If US restrictions stay focused on China rather than spreading across all surplus economies, the US orbit can still look attractive for countries able to qualify. The question is whether America uses market access as a strategic asset, or waves it around like a broken bottle. For countries trying to make multi-decade industrial decisions, that matters. A slingshot needs a sponsor that stays in place long enough for firms to build around it.

Europe is the other serious alternative. For much of EM, the EU is the only non-Chinese demand bloc large and rich enough to matter. That is why EU-Mercosur and EU-India are important beyond the usual trade-volume arithmetic. They shape whether large EMs can credibly build around an alternative market. Europe sees the China problem clearly enough. Its difficulty is speed, internal politics and the instinct to protect domestic producers first. Quite European, in other words: diagnose the problem, schedule a committee, then argue about the commas.

Developed-market protection also has an awkward side effect. Barriers in the US and Europe do not make Chinese industrial pressure disappear. They redirect it. Some flows are routed through connector economies. Some are pushed towards less-protected markets. Some Chinese value added moves one layer upstream and becomes harder to see and harder to attribute. The shield around the core can increase the pressure on the periphery.

This choice is becoming harder to blur. In the old trading system, countries could mix Chinese inputs, US demand and European standards without thinking too hard about the contradictions. Tariffs, rules of origin, export controls and security screening are making that harder. The ambiguity is getting more expensive.

That helps explain the BRICS-style hedging. Many EMs are not choosing China because they have decided the Chinese model is a warm bath of strategic benevolence. They are choosing optionality. The short-term financial and infrastructure benefits are concrete. The long-term industrial cost is diffuse, contestable and easy to defer.

Escape routes exist, but they are scarce. You need access to a large market, enough domestic capability to use it, policy that survives the next election, and a sponsor that does not decide to rewrite the bargain halfway through. That is a high bar. Most EMs will not clear it. The current pattern is therefore likely to persist. A few countries have enough thrust to break away. Most do not.

Tide or gravity

For a long period, stronger China meant stronger EM because the impulse ran through property, infrastructure and imported goods. That relationship has broken clearly enough that the old playbook is now a liability.

The commodity channel still exists. China stimulus, credit impulse and activity data still move EM assets. But a China impulse that leans into manufacturing capacity is not the same thing as one that leans into property and infrastructure. It may help some commodity exporters while tightening the noose around EM manufacturers and assembly economies. For some countries those forces offset. For others, one dominates. Models calibrated on pre-2021 data will not capture that distinction cleanly.

If this reading is right, the conclusion is harsher than “more EM dispersion”. It means lower structural expectations for a large group of countries still trying to industrialise through tradables. Some will benefit from cheaper Chinese capital goods, lower technology costs and supply-chain integration. Some will build around a genuine alternative market. Many will take in more Chinese inputs and finished goods without building much autonomous capability in return. This is the weaker medium-term development story that I think many are missing.

Generic industrial catch-up stories in exposed EMs deserve much more scepticism. The more useful question is what kind of China linkage a country has. Commodity EM and industrial EM need to be separated more carefully. Orbit-node success needs to be read through the value chain, not through gross export numbers alone. Strong exports can still hide deeper upstream dependence and a more fragile position than the headline suggests.

The slingshot and shielded cases are real, but they are scarce and contingent. Mexico has USMCA, but also a long record of turning an excellent strategic hand into disappointing income growth. Poland has European industrial integration, but also exposure to Germany’s ability to remain an industrial engine. These are better positions than most, and deserve more attention than most, but they are not automatic wins.

The practical conclusion is to lower the prior on broad EM industrial convergence where Chinese penetration is rising and little is being built locally. Raise the bar for countries claiming to be alternate manufacturing platforms. Treat shielded and slingshot cases as exceptions worth paying for.

China still matters for EM. The difference is that it now helps decide which countries can still industrialise, and which are left buying the goods they once hoped to make. It is no longer a tide. It is gravity.

Disclaimer

The contents of this note, including any analysis, opinions, and commentary, are purely for informational purposes and reflect solely the personal views of the author, Stephen Elgie, at the time of writing. They should not be construed as investment advice nor as an inducement, recommendation or solicitation to engage in any form of currency trading or other investment activities.

All information, data, and material presented in this note are believed to be accurate and reliable, yet they are not to be taken as a guarantee of future performance. The views expressed herein are subject to change without notice.

Readers are urged to exercise their own judgment and due diligence before making any investment decisions. The author and his employer, Argo Capital Management Limited accept no liability whatsoever for any loss or damage of any kind arising out of the use of all or any part of this material.

This note is not intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation.

China’s manufacturing scale is no longer just a trade story. It increasingly shapes FX regimes, commodity demand, and global liquidity transmission across emerging markets.