Strong Dollar vs. EM FX Carry

Photo by Harold Mendoza

9th June 2023

This week I discuss:

Loss of soft USD support for EMFX

Updated Themes

Updated EMFX performance including TWI performance.

Highlights from the Global PMIs

PIX system in Brazil

Turkey Update

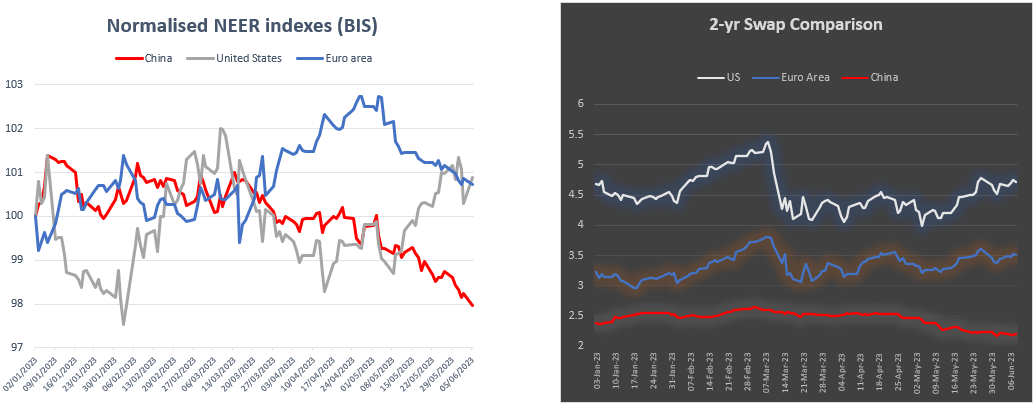

At the beginning of the year, we had a strong set of drivers for EM FX. Amongst those was the favourable relative trajectories of the EU, China and the US. We were nearing the end of the tightening cycle in the US, with growth in China and Europe expected to rebound strongly. As we stand today that constructive dynamic looks under threat from all 3 angles. Recent data out of China leaves concerns over the durability of the bounce observed in Q1, with similar concerns emanating out of the Euro Area. Following the end of the US debt ceiling charade, there is an active debate that any Fed pause could be short-lived, with patience potentially running thin over the sticky nature of core inflation and in the context of a robust labour market.

The recent broad recovery of the USD is a response to these dynamics and with quantitative tightening on the horizon it’s difficult to bet against some continuation.

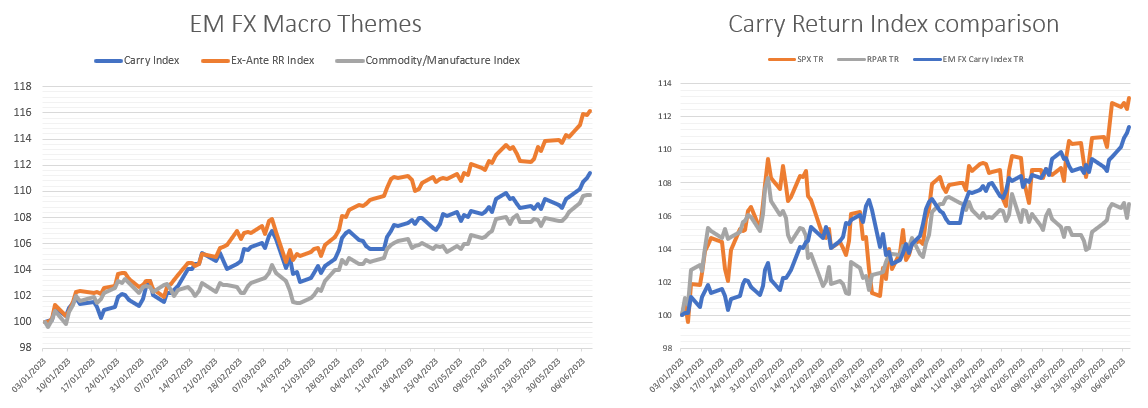

Without a soft USD backdrop, EM FX trading is a relative game, and as I’ve been discussing all year there are some strong themes in that regard. Carry and ex-ante Real-Rates based themes have already delivered strong returns, with high-yielding Latam and CEEMEA currencies performing well, and low-yielding Asian currencies under pressure. My recent expression has been long MXN and BRL and short CNH. I’ve taken off most of these core positions in the near term, but I’ll continue to trade tactically in that direction. I mentioned 2 weeks ago that I would use the resolution of the debt ceiling to take profits on EM FX longs, as I anticipate some fears to re-emerge over the path of US disinflation. With so much relative strength already observed, I think it’s worth being patient.

Above (left) we can see the strong total returns of 3 themes. The right-hand chart shows how my expression of carry has performed against US equities, and against a risk parity measure. I expected risk parity to do well in 2023 after heavy losses in 2022, and that view remains a foundation of a medium-term constructive view on EM FX. A decline in US recession odds has occurred over the past month, and judging by equity performance, markets may judge this decline to be more meaningful that rising fears over further Fed tightening.

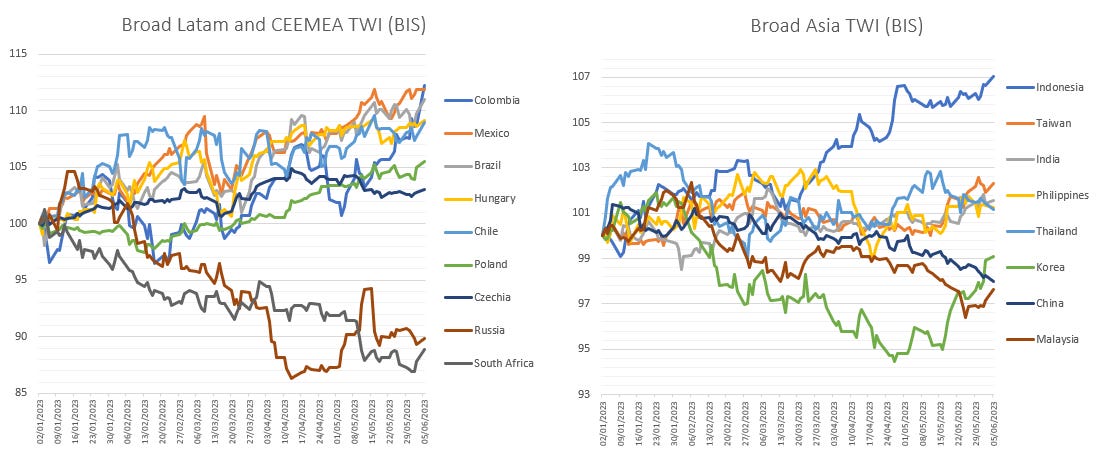

TWI performance

Periodically I review EM FX performance on a TWI basis as it has the potential to give clearer insights. Here you can most clearly see the recovery of the Korean Won, despite only tentative signs of recovery in exports. This could be mere mean reversion after such a sustained period of relative weakness, something I flagged some weeks back but shamefully failed to pull the trigger on. A similar dynamic is visible in the Taiwanese Dollar. It would be easy to imply significant optimism over tech exports, but as far as I can see, the jury is still out there.

Macro data notes

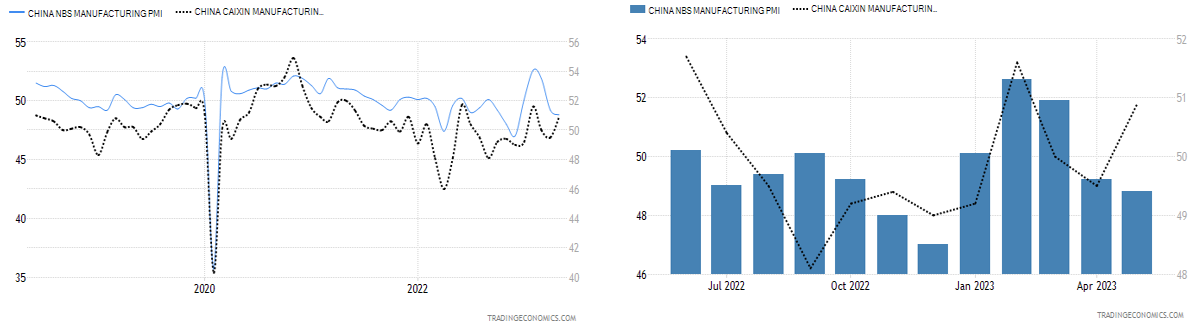

In China, we had conflicting signals from the PMIs. First, the NBS manufacturing PMI came in soft. This was followed by much stronger than expected Caixin PMI. This latter reading was strong enough to materially boost the global manufacturing picture in the S&P series. I’ll cover the global PMIs in their own section

In Brazil, headline CPI came in below expectations at .23% MoM, with core rising 0.37%. Disinflation looks on course there. The same can be said of Mexico, where headline inflation fell by .22% MoM, with core inflation rising slightly less than expected at .32%.

In the US, we had another solid yet mixed jobs report with the 339k headline surprising alongside upward revisions. There were falls in weekly hours and wages together with a rise in the unemployment rate to 3.7%

The most recent US initial claims print yesterday saw a jump to 261 raising the 4-week average to 237.25. With the multiple head fakes observed in employment data in recent months, most of us will wait for some reinforcement of this signal before reading too much into it.

Central Banks

In what should be the drumbeat of the summer, all but one EM central bank kept policy unchanged in recent meetings. The use of copy and paste was significant from the NBP in Poland, with rates set to remain at 6.75% for the foreseeable future. In India, the RBI kept rates at 6.5% despite recent encouraging inflation prints. Activity has been strong recently in India and the central bank did strike a hawkish tone. To buck the trend, the Bank of Thailand raised rates by a quarter point to 2%. They held back in recent months, to observe the evolution of the DM banking stress. They seem to view these risks to have passed.

Next week we have a meeting in Taiwan, where no change is expected.

S&P Global PMIs

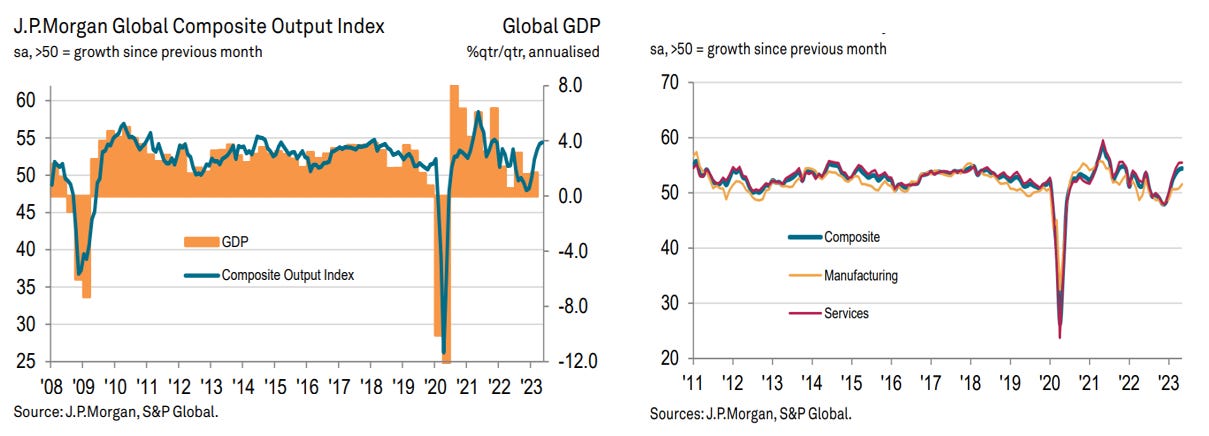

These reports kick off each month and seem to be the best forward-looking indicator we get. I lifted the below charts from the reports that S&P posted on their website (spglobal.com). As we can see the global composite is strong and we still have the divergence between the goods and services sectors.

Services are still in a recovery phase from the pandemic which has created an unusually large divergence, certainly in the history of these series.

The global manufacturing print is heavily supported by a strong China number I discussed earlier.

Within the global composite, there is data that can give us insight into the inflation picture. The index for Input Prices fell from 58.5 to 56.7 and the index for Output Prices fell from 54.9 to 54.4. Measures of goods inflation are normalising, whilst services measures continue to be sticky.

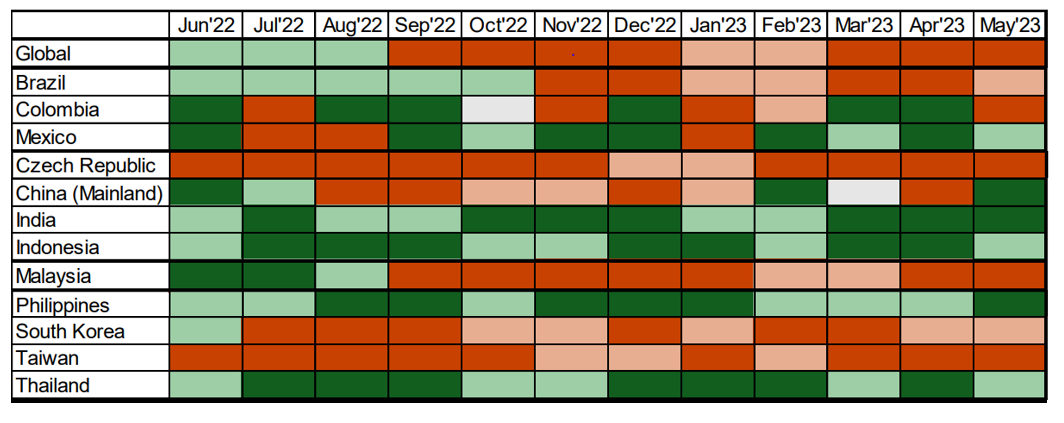

S&P produce manufacturing PMIs for the majority of the countries I cover in these notes, and I’ve reconstructed the relevant elements of their heatmap.

As I mentioned a few weeks ago in my Asia focus piece (Asian FX Focus), these have given a good signal for EM FX RV.

Turkey FX

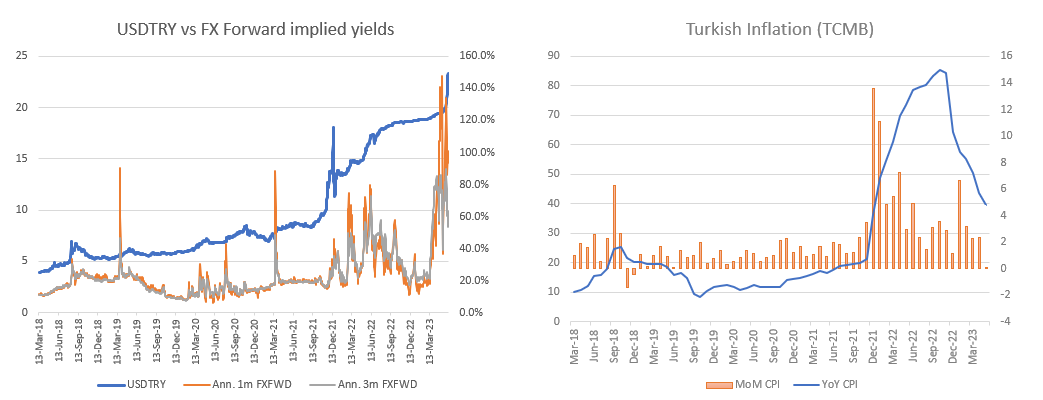

I wrote about Turkey in more detail between the rounds of the recent election. (Let’s talk Turkey). As predicted in my pessimistic note, spot USDTRY has marched higher since the conclusion of the election. I don’t have visibility on liquidity, but judging from the FX forwards, I can only imagine the chaos. The passthrough from such rapid depreciation is going to further challenge the domestic inflation picture.

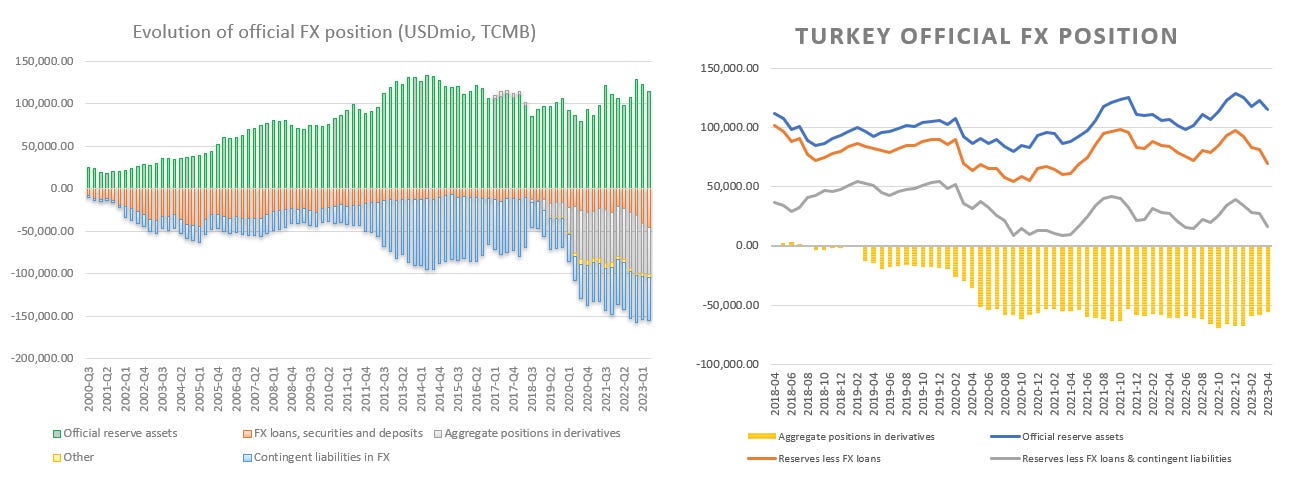

We don’t have the May data for reserves yet, so all we can do is reflect on the pre-election state of affairs, with a central bank effectively short USD in the midst of a currency crisis. Short of a full-scale epiphany by Erdogan I’m a seller of bounce in TRY on the back of a move to a more orthodox policy.

A note on PIX

At a recent event in London, an employee of Banco de Brasil showed me how the PIX instant payments system (bcb.gov.br) operates. As in India with their successful Unified Payments Interface (UPI), the power of secure mobile banking that provides access for the previously unbanked is very powerful. There are benefits in crime reduction, productivity for banks who don’t need to drive as many armoured trucks around the country to fill up ATMS, and benefits to the tax revenues of digitising grey economy activities. My UK banking apps looked poor in comparison with what my Brazillian friend had at his fingertips. Using PIX, the simple scanning of a QR code does the bulk of the work in making an instant payment. Cryptocurrency bears will point to these systems as fulfilling one of the original use cases of Bitcoin, although those who crowdfunded a pro-Bolsonaro insurrection using PIX might be uncomfortable with the lack of anonymity.

Market Monitors

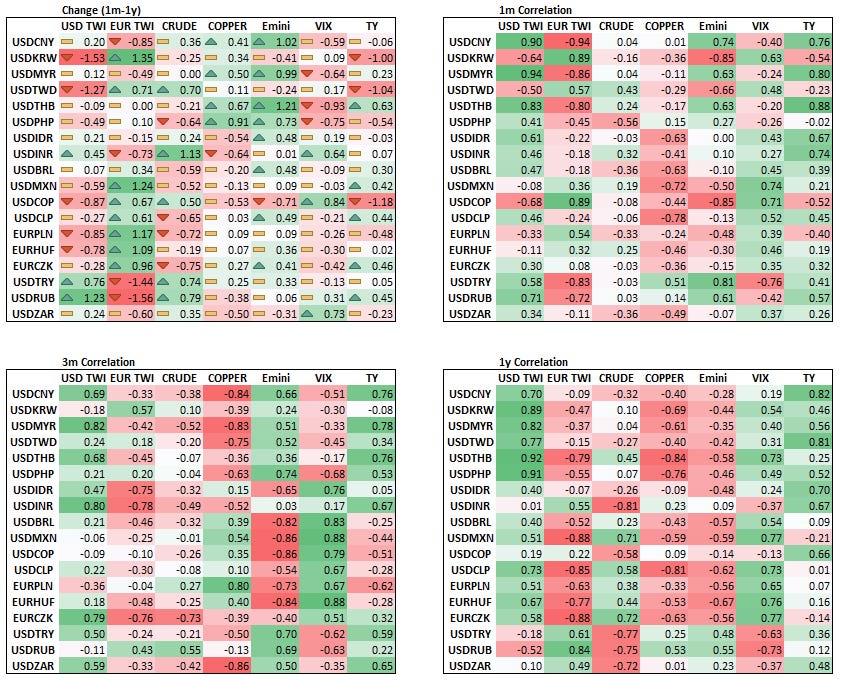

Correlation

KRW and TWD are diverging from broader USD/ASIA. EUR/CEE's historical correlation to the EURTWI has broken down of late. EUR/CEE can often be inversely correlated with the EURTWI, with strong EU macro developments driving local currency outperformance in CEE.

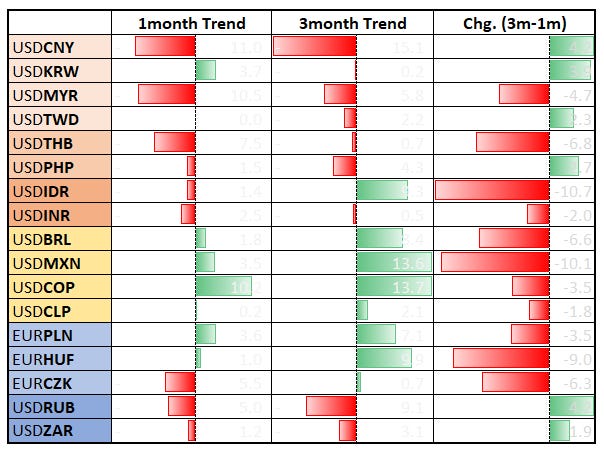

Trends

Carry currencies are maintaining some medium-term trend strength with COP the short-term stand out. Overall, short CNY vs the USD is still the strongest trend.

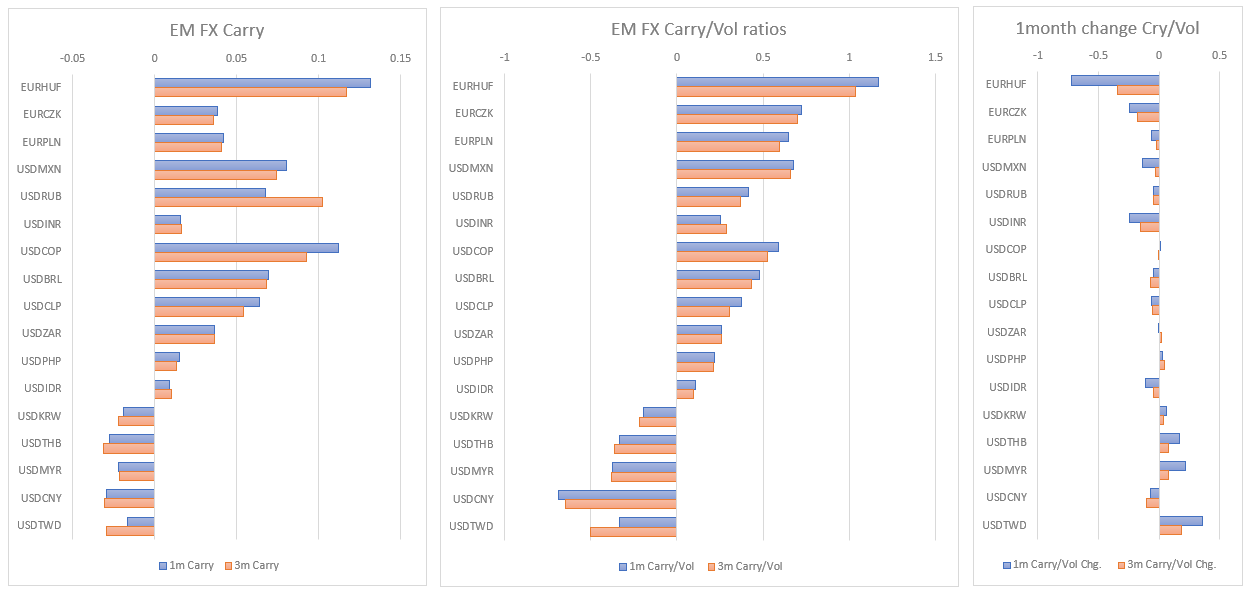

Carry

No major changes in the last few weeks. The post-NBH fall in HUF carry doesn't come close to taking it off the top spot.

Signing off

Thanks for taking the time to read this note. These notes cover my personal thoughts on markets and macro from outside of the industry. Any thoughts and feedback from those closer to the action would be appreciated.

As always, please share the note with anyone you feel might enjoy it.

In the meantime, if you’re trading, be disciplined and be lucky,

Stephen