Hegemon Without Discipline

USD and EMFX Macro implications of the Iran War

Just as macro traders had settled into the latest cottage industry of becoming temporary experts on AI, hyperscaler capex and the vulnerability of EM services exporters, a much older threat reasserted itself. We pivoted abruptly from the socialisation of cognitive labour to the price of oil, the security of shipping lanes and the familiar tyranny of energy dependence.

In the early phase of a shock like this, you can’t get the fundamental playbook out too early. It’s all about positioning. Long EM. Long gold. Short dollar. They made sense, but were crowded. We’re rarely fast and ruthless enough with our favourite trades, and this is another lesson in that.

After the initial moves, we began to see the usual higher oil terms of trade dispersion. With what now looks on the charts to be a significant lag, rates markets began to price renewed inflation pressure and tighter policy constraints. Unwinds and old habits produced a dollar bid, but I think it is less convincing on fundamentals. In amongst the pain, the reality is that the issuer of the reserve currency is behaving less like the steward of a system and more like the biggest source of risk within it.

At the centre of this mess is an American president who appears too vain, too impatient and too cognitively lazy to absorb even a moderately complex chain of consequences, yet retains enormous power to unleash one. He ignored the most obvious second-order risks around Hormuz, energy infrastructure and oil, then seemed to expect the allies he has spent months insulting to help contain the fallout. On Liberation Day, the world discovered that the supposed guarantor of the system was being steered by an orange pensioner who neither grasps the facts nor cares much for the discipline of mastering them. He has since graduated from terrorising global trade to waging an illegal war and threatening the global energy system, apparently no more troubled by the collateral damage to poorer nations than he was by the human costs of the USAID rug-pull.

America still retains the advantages of scale, geography, energy and incumbency. Those do not disappear because the executive is erratic. But once the first-order effects fade, the dollar will likely take another reputational hit. The United States still has the power of a hegemon, but increasingly lacks the seriousness of one.

This note is a post-mortem on the initial reaction and an attempt to separate fragility from positioning. I look at how EMFX actually behaved through the sell-off, where the terms of trade shock mattered and where it did not, why another inflation pulse is awkward for an EM complex that is no longer broadly cheap, and which trades may make sense on any normalisation. I then turn to two case studies: Egypt versus Turkey as competing carry expressions, and Hungary as a potential political asymmetry. There is every chance that some of these ideas hit a tethered mine in the weeks ahead, but it still seems worth taking stock.

Positioning first, then some fundamental follow through

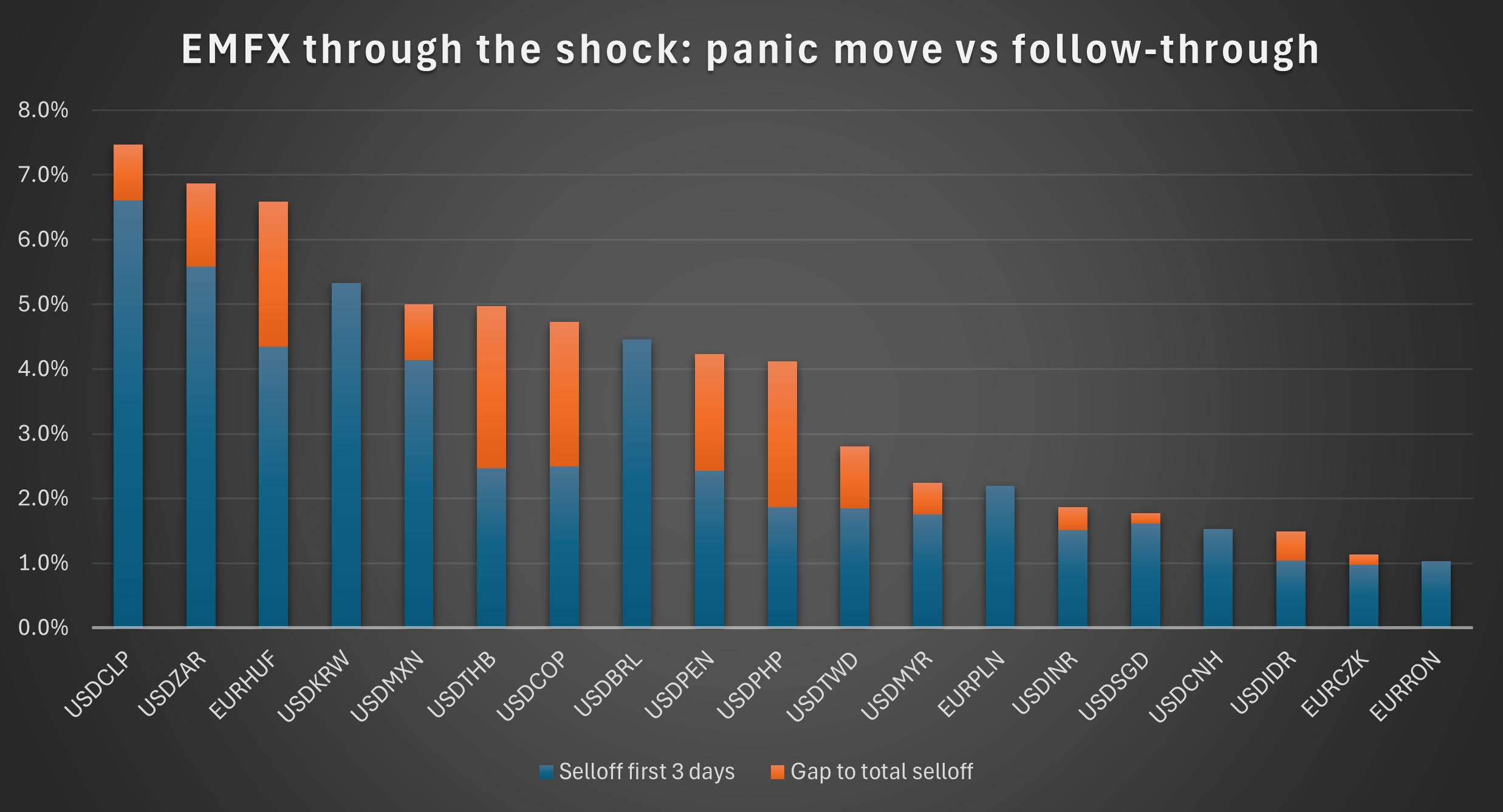

The initial move was mostly a standard oil and de-risking shock. Importers sold off, the dollar caught a bid, and liquid EM proxies were hit first. In several cases, most of the damage was done in the first three days.

That front-loaded pattern is useful. BRL is the clearest example: a large early move, but limited extension afterwards. KRW and MXN fit the same broad category. These look more like fast pricing of the obvious, helped by liquidity and positioning, than a slow discovery of deeper local problems.

The more interesting cases are the ones where the move kept extending after the initial panic. THB stands out. HUF does too. There, the market appears to have moved beyond generic de-risking and started to price something more specific.

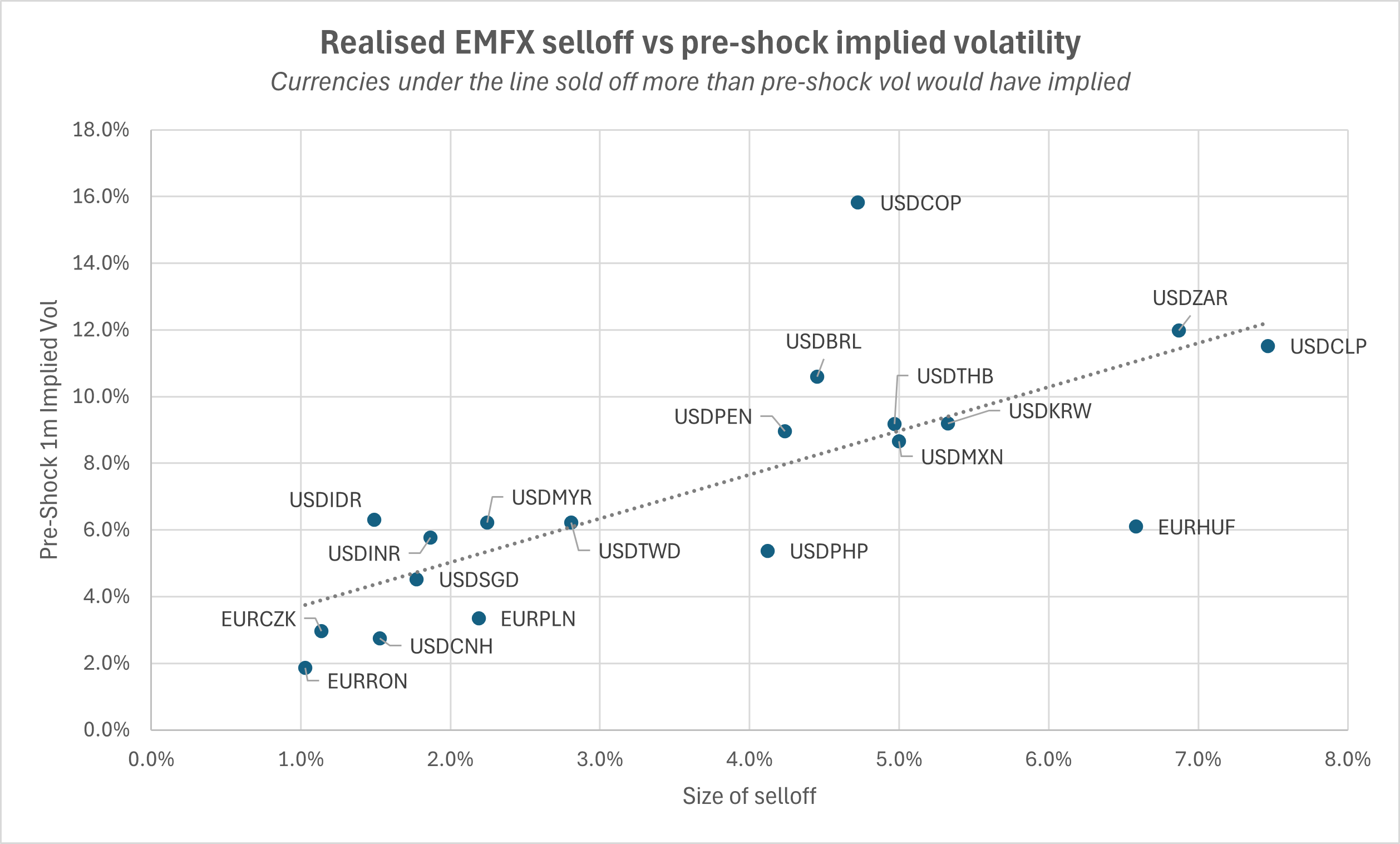

Comparing realised sell-off with pre-shock implied volatility gives a rough sense of what was already in the price. ZAR and CLP sold off hard, but not in a way that looks wildly inconsistent with the vol already embedded. HUF looks more notable on this basis. COP came into the year flagged as expensive with election risk, and therefore unlikely to be a major long in most macro books. More managed names like CNH and INR look calmer, though that says as much about policy management as it does about underlying strength.

Three broad buckets emerge. Front-loaded washouts where the market hit liquid risk quickly. Names where the commodity shock was painful but not especially surprising. And currencies where the follow-through was larger and the market appears to have repriced a more local problem. Brazil looks closer to the first category. Thailand and Hungary look closer to the third. In Hungary’s case, FX sold off early, but the more telling move came later as local rates got hit. Early-year bond buying in anticipation of a positive election outcome will have been unwound with a lag, giving a second wind to the HUF selloff.

Commodity shock to an established terms of trade trend

The chart below shows the recent shock against the prior twelve month backdrop. The starting point matters as much as the move itself.

Some countries had been riding a significant positive terms of trade shock for the past year. The oil shock dilutes the highly positive trajectory for Chile, while Brazil and Colombia got tailwinds.

Korea and India had already seen a negative twelve month terms of trade move before the conflict began, and the recent shock adds to it. For Korea, the valuation argument and the chip cycle catalyst were working to offset its negative commodity backdrop. India had no such tailwinds going in, and now it’s only the central bank keeping the beta low.

Thailand is also negative on both time horizons, and gets an extra black mark from tourism exposure.

South Africa gets hit by the oil move, but also the speculative precious metal unwind. This gives it a worse looking outcome than we might have expected on day one.

The broad point is that this shock hit an EM complex with trending and divergent terms of trade dynamics. For several countries, the recent move is compounding a problem that was already building. That distinction matters when you come to look at where the valuation cushion actually exists.

USD: the smile returns, briefly

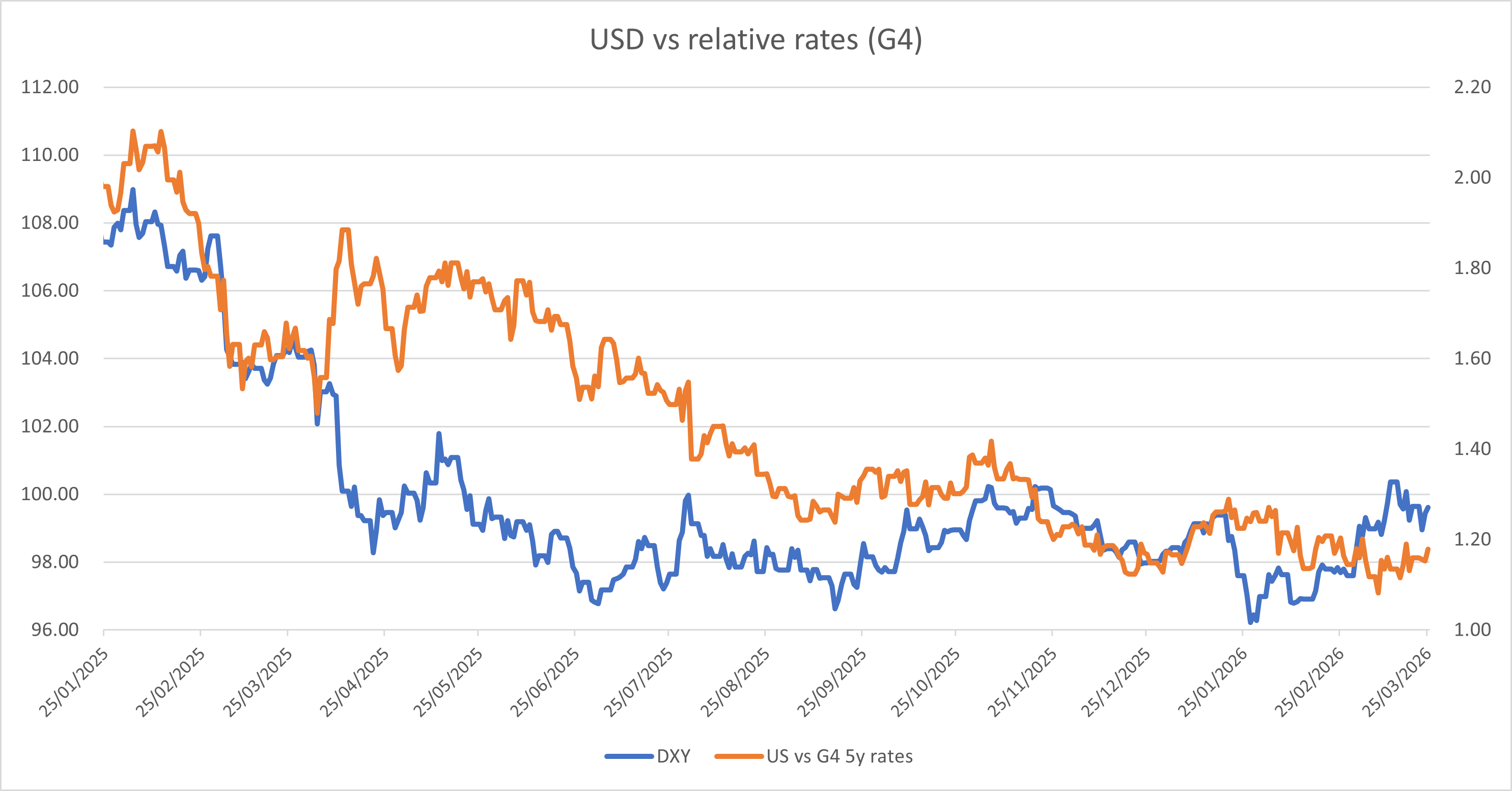

In my January note, I laid out a four-pillar framework for the dollar: macro pricing inputs, risk regime and positioning, credibility and politics, and external financing. It is worth keeping that map close for what follows, because this episode has moved more than one lever at once.

The relative rates divergence that followed Liberation Day has been gradually reasserting itself since. The tariff shock was the period where pillar three, the governance discount, got embedded in the price. The dollar underperformed its rates signal because the shock was domestic. People drew the right conclusion and got short.

The Iran shock has temporarily changed that. Safe haven demand, oil terms of trade support and relative insulation from a shock that originated outside the US have all pushed the dollar beyond what relative rates alone would justify. The USD smile logic is back, which is something we had not seen work cleanly for a while.

The tactical dollar bid has a fundamental underpinning here too. If you were designing a developed economy to weather an oil shock originating in the Middle East, you would design something close to what the US currently looks like. It is a large net energy producer and it has no meaningful shipping lane exposure in the Gulf. The US equity market has been losing its structural bid from foreign investors, but that process does not accelerate on an oil shock alone. It needs recession risk to really move, and that is not the base case yet. The relative story is genuine, and the dollar rally reflects that.

The question is how much further it runs from here. The soft USD momentum that built post-Liberation Day left a lot of people selectively short, and a geopolitical shock is a fairly efficient way to flush that out. Some of this move is that, rather than a genuine reappraisal. The governance questions that were sitting in the price before the conflict have not been answered. They have just been briefly drowned out. The man running the world’s reserve currency is the same man who triggered the energy shock in the first place. That is not a normal risk regime. When the noise settles, those questions will still be there, and pillar three will matter again. The hegemon lacks discipline, and looks hostage to one man in a way not seen in modern times.

EMFX is not cheap enough for another inflation pulse

I made this argument in January and it bears repeating, because the oil shock has made it more pressing. EMFX is no longer broadly cheap in the way spot charts tempt people to believe. Much of the nominal weakness people remember from the past few years has already been offset by inflation differentials. Currencies that still look optically low in spot are often much less cheap once you look at the real effective exchange rate, and an oil shock adds another layer to that problem for importers. A fresh inflation pulse on top of valuations that were already less forgiving than they looked means the cushion investors might assume is there after a sell-off is smaller than it appears.

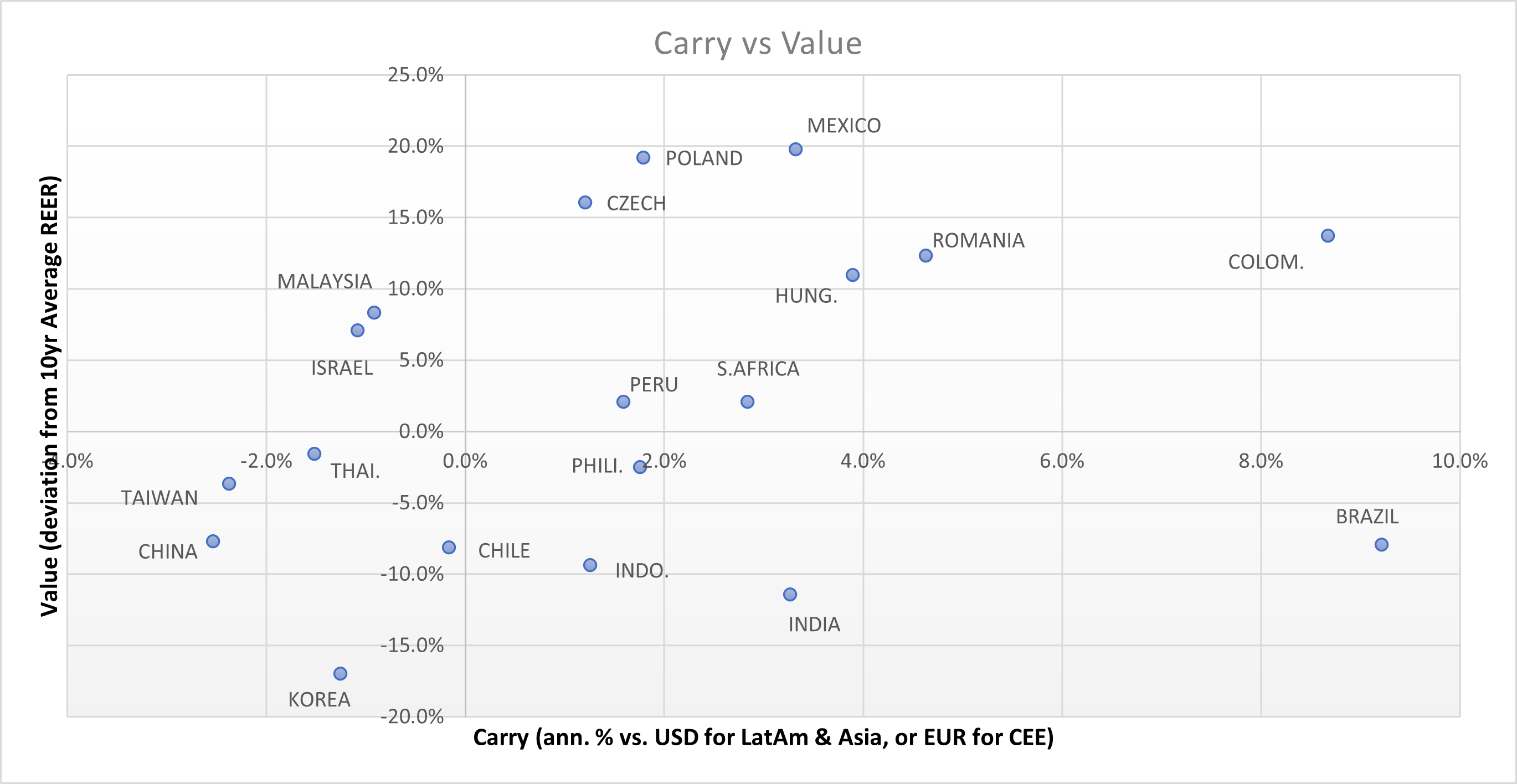

The carry and value chart below is the right place to start. The good quadrant is obvious: cheap currencies with carry.

Reading that chart after an oil shock, the first question is which markets still offer a credible real return once you factor in what the energy pulse does to the inflation path. That is what the ex-ante real rates chart adds. These levels will be flattered by the failure of economists to update their forecasts on a timely basis, worth bearing that in mind, but for now it's all we've got.

Brazil is the clearest case where both charts point the same way. It screens cheap on carry and value and sits at the top of the real rates chart with ex-ante real rates approaching 10% by 2027. The recent sell-off looks more like a positioning event than a genuine loss of the medium-term story. The fiscal concerns are real and worth monitoring, but at current valuations and with that real rate buffer, the burden of proof sits firmly on the other side.

Korea remains an interesting relative long. The current account is healthy, the REER is cheap, and there are plausible flow catalysts later in the year, including potential WGBI inclusion. Supply disruption and shipping uncertainty tighten semiconductor availability and will inflate prices further. Firming chip prices flow directly into the current account, and that effect does not require a demand recovery to show up. Korea’s BoP advantage will assert itself as soon as conditions stabilise.

CLP is a different kind of case. The frustration with Chile last year was that the copper story translates slowly into currency gains, partly for reasons I laid out in January around income balance leakage and foreign ownership of the mines. But the quality of the demand driver has improved. China’s property cycle was an unreliable engine for copper. The AI infrastructure buildout is more durable, and the capex commitments behind it are not going away because of one geopolitical shock. On the real rates chart Chile sits in the middle of the pack, not exceptional but not problematic either. Layered on top of the copper story is a reformist government whose policy direction the market had begun to price before the conflict interrupted. That re-rating has been paused rather than cancelled, and when calm returns both threads should reassert themselves.

India looks more vulnerable on multiple fronts and the carry is not sufficient compensation in this higher vol environment. The BoP exposure to this conflict includes oil imports, LNG, export receipts from the Gulf region, remittances from the large Indian diaspora in the Middle East which are a meaningful current account support in normal times, and a potential reduction in FDI. The RBI’s management of the exchange rate means we get an artificially easy exit on INR longs or a managed entry point on shorts.

Thailand barely registers positively on either chart. Low carry, not cheap on REER relative to its own history, and facing an awkward imported inflation problem with limited policy room to absorb it cleanly. The untimely removal of fuel subsidies acts as a local force multiplier. Thailand’s BoP is usually boosted by tourism, and a prolonged conflict with elevated jet fuel prices and heightened travel risk aversion is not a benign backdrop for inbound flows. With the carry working against you and the REER offering no cushion, THB looks less like something to avoid and more like a relative short against something like KRW.

The broad point is the same one I made in January but with more urgency behind it now. Valuations aren’t helping many longs, and will be eroded by another inflation pulse. The burden of proof for EM longs beyond their short term beta to de-escalation should be high.

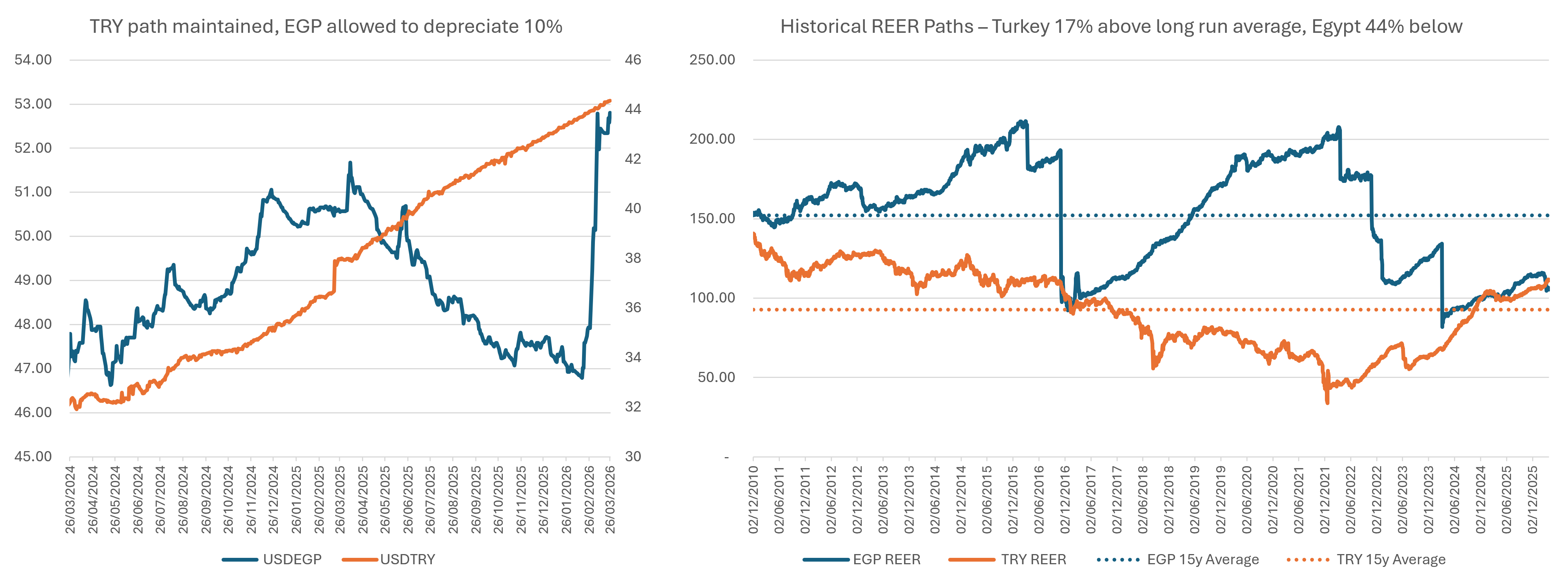

Egypt versus Turkey: divergent management of the two favourite frontier carry trades

Both countries lose on an oil shock. Egypt is additionally more exposed to food inflation, given its reliance on imported wheat and the political sensitivity of bread prices. Two losers with different adjustment styles.

Turkey chose to defend the path more aggressively. That’s not surprising as it’s the linchpin of their disinflation efforts. A major investment bank estimates that between 27 February and 23 March, the CBRT’s net foreign assets excluding swaps fell from around $70 billion to $20 billion, with roughly $34 billion reflecting FX intervention to support the lira and the remainder largely gold price moves. Gross reserves including gold were still around $161 billion as of 23 March, so this is not a story of immediate exhaustion. But the usable liquid FX stock is much smaller than the gross number suggests, something closer to $25.5 billion once you strip out gold, swaps and IMF SDRs. Recent large gold sales reinforce that picture.

Egypt is harder to read on a timely basis. The adjustment is filtered through state banks, Gulf funding and the wider sovereign financing apparatus. What is clear is that Egypt entered the episode with stronger buffers than in past stress events. Net international reserves were $52.75 billion at end-February, net foreign assets had risen to a record $29.5 billion in January, and the IMF completed reviews in late February that unlocked around $2.3 billion.

That matters for the trade. Turkey still screens as the cleaner vol-adjusted carry story. One-year implied gross carry is around 40% and expected net yield around 20% if the path is maintained. Egypt’s NDF curve offers an outright yield closer to Turkey’s expected net yield. If markets normalise, initial TRY gains would come from compression in the forwards. In EGP, there is also room for some yield compression, but also for a reversal of part of the recent 10% spot depreciation. By allowing more volatility and a spot adjustment, Egypt has changed the calculus for existing and future positioning, leading to lower outflows and more near term appeal.

Valuation leans the same way. Turkey still looks rich enough that the burden of proof is higher. Between the two, I prefer EGP.

Hungary: a political trade, briefly interrupted by oil

Hungary is one of the few places in EM where the political catalyst is tangible enough to matter outside of this current mess. The 12 April parliamentary election is widely seen as the most consequential in years. Péter Magyar’s Tisza party offers a plausible improvement in Hungary’s relationship with Brussels, with knock-on effects for EU funding, sovereign risk premia and the HUF.

Polls point to a close contest once you factor in Hungary’s mixed electoral system with a constituency map that favours the incumbent. Tisza will need to win the popular vote by 5-10% to take power. The balance of polls suggests they have a better than even chance as things stand.

Before the Middle East shock, Hungary had become a fairly consensual trade. The view was that an Orban win would see a contained reaction, with some suggesting a fresh term may still force some normalisations with the EU from both sides. Unfortunately, Iran smashed up well reasoned positions, but that de-levering is part of what makes Hungary more interesting again.

The NBH’s March communication matters here. After cutting the base rate to 6.25% in February, it held in March and pointed explicitly to the Iran conflict, higher energy prices and renewed global inflation risks. It also stressed FX stability as crucial for anchoring inflation expectations and reiterated its commitment to positive real rates. If the shock threatens to feed inflation through energy and the currency, the central bank’s first instinct is to preserve the buffer, not to keep cutting.

The election trade cannot become crowded again given the proximity, while the upside remains meaningful. CEE offers little elsewhere, with expensive energy-exposed currencies across the board. Hungary stands out as the most interesting long.

The global saboteur

My earlier notes argued that Trump had become a saboteur of the United States. He has since found a way to expand the franchise. He has moved from vandalising trade relationships and institutional credibility to threatening the global energy complex itself, with the predictable consequences landing furthest from Washington. Tariffs were at least on the tin. This was not.

That matters for the dollar. In the first phase of a shock like this, the USD can still rally on oil, fear and relative insulation. If we are lucky enough to move into something calmer, I would be inclined to drop the USD like a hot piece of Trump’s Beautiful Clean Coal. The market has a habit of eventually pricing the defects of the executive, not just the immediate mechanics of whatever crisis he has generated.

The United States still has the power of a hegemon. Energy production, deep markets, reserve-currency incumbency. None of that is gone. But the man at the centre of the system is actively degrading the franchise behind it, and that is not the foundation for an extended dollar bull story. We’re the wrong side of the midterms for one of those.

Signing off

Thank you for reading. Feedback is always welcome, and so are disagreements.

These notes exist partly to keep the thinking sharp between the noise of daily markets, and partly to stay connected with people worth staying connected with. If that is you, feel free to reach out.

As always, if you’re trading, be disciplined and be lucky.

Stephen

Disclaimer

The contents of this note, including any analysis, opinions, and commentary, are purely for informational purposes and reflect solely the personal views of the author, Stephen Elgie, at the time of writing. They should not be construed as investment advice nor as an inducement, recommendation or solicitation to engage in any form of currency trading or other investment activities.

All information, data, and material presented in this note are believed to be accurate and reliable, yet they are not to be taken as a guarantee of future performance. The views expressed herein are subject to change without notice.

Readers are urged to exercise their own judgment and due diligence before making any investment decisions. The author and his employer, Argo Capital Management Limited accept no liability whatsoever for any loss or damage of any kind arising out of the use of all or any part of this material.

This note is not intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation.

Geopolitical shocks like this usually transmit through the dollar and financial conditions first before they show up fully in growth expectations.

That’s often why EMFX reacts earlier than equities. It sits closer to the liquidity and funding channel.

Watching whether the move tightens global financial conditions from here is probably the key regime signal.

Excellent & Sharp Commentary Stephen Sir.